By Glenda Taylor

If your most recent property tax assessment caught you by surprise, you have options beyond simply paying it. With a little research and a lot of determination, you can get your property taxes lowered. Here’s how.

1 Lower Your Tax Bills

Property tax rates are decided at the county level, and the money collected is used to pay for schools, streets, and public safety. If you want to own a house, you already know that you’re probably going to have to pay property taxes. What you may not know is that you might be able to decrease the amount of taxes you owe. So, don’t just fume about a high tax bill—do something. Scroll through to discover ways to lower your property taxes and keep more of your hard-earned money for yourself.

2 Review Your Property Tax Card for Errors

Your home’s tax card is the official record of your property. It contains information such as your home’s assessed value, square footage, the year it was built, and the number of bedrooms and bathrooms it has, but tax cards often contain errors. Obtain a copy of your tax card from your local county assessor’s office and go over it carefully. If you find errors—if, for instance, it lists more bedrooms than you actually have—point that out to the assessor and ask for a reevaluation of your tax.

3 Appeal Your Tax Valuation—Promptly

Most county assessors limit the amount of time you have to appeal your tax valuation after they mail out notices; in some jurisdictions, the period is as little as 30 days. If you fail to appeal within that time frame, the window of opportunity closes, and you’ll have to pay the higher tax. The appeal process typically involves filling out a form detailing why you believe the assessor’s valuation is too high—for example, perhaps the house has sustained structural damage.

4 Get Rid of Outbuildings

Structures on your property, including storage sheds, she-sheds, and greenhouses, may also be assessed for taxes. That said, some counties and towns tax only permanent structures with foundations, or only those above a certain size. But if your property tax bill includes a couple of storage sheds that you don’t really need, consider getting rid of them. If you decide to remove them, notify your county assessor’s office so it can update your property tax card.

5 Check to See If You Qualify for Property Tax Relief

Not all states offer property tax relief, but many do offer reductions for homeowners who are seniors, veterans, or disabled. In addition, certain types of property, such as property used for agricultural purposes, may qualify for tax breaks. These reductions are decided at the state level, but you won’t automatically get them—you need to apply. Call your county assessor’s office to find out if you qualify for any tax relief programs.

We use QuickBooks daily in our rental property business!

It’s used to invoice tenants for their rent, track expenses by property and unit number, and our tax advisor can log on anytime to get information he needs for processing taxes or analyzing our data for goal setting meetings! QuickBooks is the #1 accounting software for small businesses, and today you can take advantage of 30% off your first 6 months of QuickBooks Online using our exclusive Business Affiliate link

6 Move to a Less Expensive Area

Property tax rates vary widely from state to state and from county to county. If you live in a county with high property taxes, you may be able to buy a house in a neighboring county and pay much less in property taxes. You may end up with a longer commute, but you’ll save on taxes.

7 Compare Tax Cards of Similar Homes

If you’re sure you’re paying more than you should in property taxes, you stand a better chance of having your tax lowered if you can demonstrate that houses similar to yours are being assessed at a lower value. Tax cards are public information, so go through the ones of homes like yours (same square footage, age, style, and number of bedrooms and baths). If you can show that your property is valued higher than other similar properties, the assessor’s office may reduce your valuation.

8 Have Your Property Independently Appraised

County assessors and real estate appraisers value properties in different manners, but if a real estate appraiser values your home at less than the county assessor does, you can often get your valuation reduced. You’ll pay $250 to $400 for an independent appraisal, but if it substantially reduces your home’s assessed valuation, you could save thousands every year.

9 File for a Homestead Exemption

A homestead exemption provides tax relief for a primary residence in the wake of a bankruptcy or death of a homeowner. Many, but not all states, offer homestead exemptions, but requirements vary. You typically have to have lived in the house for more than a year and must meet certain income requirements. If you qualify, the county assessor will be able to tax only a portion of the value of your property.

10 Invite the Assessor Over

Sometimes the best way to show the assessors that your house is not worth as much as they claim is to ask them to come see for themselves. The key here is to accompany the assessor and point out all the problems she may not notice, such as cracks in the foundation, structural problems, water damage, and other significant defects.

11 Hire an Expert

Navigating the appeal process can be complex and time-consuming. Fortunately, if you’re not up to it, there are experts who can help. Both tax attorneys and property tax consultants can challenge your property valuation to get your taxes reduced. You’ll have to pay a tax attorney up front for the time spent on your case, while a property tax consultant takes a cut of your tax savings, usually 50 percent of the first year’s savings.

Pay Less

Who doesn’t want to pay less in property taxes? With this advice in hand, you can begin the process of lowering your property taxes.

provided by bobvila.com

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

As a landlord or property manager, understanding the intricacies of smoking policies in rental properties is crucial. This comprehensive guide dives into the multifaceted aspects of managing smoking tenants, including legal considerations, tenant rights, and practical enforcement strategies.

Legal Landscape: Smoking and Protected Classes

Understanding the legal aspects of how smoking is treated in the context of rental properties is crucial for landlords and property managers. Here’s a more detailed look:

Fair Housing Rules and Smokers: The Fair Housing Act, a pivotal piece of legislation in the United States, aims to prevent discrimination in housing. It enumerates specific protected classes, such as race, religion, national origin, sex, disability, and familial status. Smokers do not fall within these categories. Courts across various jurisdictions have upheld this view, clearly indicating that landlords are within their rights to impose no-smoking policies without fear of violating fair housing laws.

State-Specific Smoker Protection Laws: While federal law does not protect smokers, there is a patchwork of state-level laws that offer varying degrees of protection to smoking tenants. In 29 states and the District of Columbia, laws have been enacted that classify smokers as a protected class, to some extent. These laws vary significantly in their scope and application. They may, for instance, prevent employers from discriminating against smokers but do not necessarily apply to housing. Therefore, it’s important for landlords to be aware of the specific laws in their state and how they might affect their ability to enforce no-smoking policies.

Differences in Enforcement: The application and enforcement of these state laws can significantly differ. In some states, these protections are robust, while in others, they are more symbolic. Knowing the nuances of state law is essential for landlords to navigate this landscape effectively.

Tenant Rights and Smoking Regulations

The rights of tenants regarding smoking in rental properties are also a complex issue:

Absence of Federally Protected Smoking Rights: At a national level, no law explicitly grants tenants the right to smoke in rental properties. This absence of federal protection means that, generally, landlords have considerable leeway to restrict or prohibit smoking on their properties without infringing on tenants’ legal rights.

Fair Housing Act Considerations: It’s critical to understand that the Fair Housing Act’s primary goal is to prevent discrimination against protected classes. Since smokers are not a protected class under this act, landlords are not discriminating based on this law when they prohibit smoking. This distinction is important because it allows landlords to implement no-smoking policies as a part of their property management strategy without the risk of legal challenges based on federal discrimination laws.

Impact on Tenants’ Health and Safety: The decision to prohibit smoking is often rooted in concerns about health and safety. Secondhand smoke can pose significant health risks to non-smoking tenants. Similar to noise complaints, smoking can be a source of disputes and discomfort in multi-tenant properties. By restricting smoking, landlords are often seen as taking steps to ensure the health and well-being of all their tenants.

Local and State Regulations: Besides federal law, local and state regulations can have a substantial impact on smoking policies in rental properties. Some cities and states have more stringent regulations that may restrict smoking in certain types of housing or areas. Landlords need to be aware of these local ordinances as they can further define what is permissible regarding smoking in rental properties.

Need a Lease Agreement?

A FREE account gets you access to over 200 free forms. Upgrade to a paid account (monthly, annually, or lifetime)

EZLandlord Forms Is Offering 15% 𝙊𝙛𝙛 For New Customers!

We cannot recommend these guys enough!

👉 State Specific Leases 👉 400 Forms to make your landlord-tenant relationship top notch 👉 200 FREE forms for those not ready to purchase 👉 4.8 Rating with over 5000 Reviews 👉 Pro Members get access to ALL leases and forms for $12 per month OR $75 if you purchase the annual membership 👉 YOU CAN BUY LIFETIME FORMS for $399

USE CODE 𝐒𝐓𝐀𝐂𝐈𝐄𝟏𝟓 to get 15% OFF ALL first-time purchases, EVEN THE LIFETIME FORMS!

Implementing and Enforcing No-Smoking Policies

Incorporating No-Smoking Clauses in Leases: Clearly defined no-smoking clauses in lease agreements are pivotal. These should explicitly state the restrictions and consequences of violating the no-smoking policy.

Uniform Application and Enforcement: To avoid discrimination claims, it’s imperative that no-smoking policies are applied uniformly to all tenants. Consistent enforcement is also key to maintaining the policy’s integrity and effectiveness.

Managing Existing Tenants Who Smoke

Approaches to Monitoring and Compliance: Employing smoke detectors specifically designed to detect cigarette smoke can aid in monitoring compliance. However, privacy concerns must be taken into account, especially when using security cameras in common areas.

Addressing Violations and Potential Eviction: When a tenant breaches a no-smoking clause, landlords typically begin with a formal warning. Continued violations can lead to eviction processes, contingent on the terms outlined in the lease agreement.

The Case of E-Cigarettes and Vaping

Extending Policies to Include Vaping: As e-cigarettes and vaping become more prevalent, landlords should consider updating lease agreements to encompass these forms of smoking. The effects of vaping on property and other residents can be similar to traditional smoking.

Practical Tips for Landlords

Clear Communication: From the onset, landlords should communicate their smoking policies clearly to prospective and current tenants. This ensures that all parties are aware of the rules and their implications.

Legal Consultation: It’s advisable for landlords to consult legal professionals, particularly when drafting no-smoking clauses and policies, to ensure compliance with local and state laws.

Handling Exceptions and Accommodations: While enforcing no-smoking policies, landlords should also be prepared to handle exceptions or requests for accommodations in a fair and legal manner.

Conclusion

In summary, tenants who smoke are generally not considered a protected class under federal law, specifically the Fair Housing Act. This means landlords have the legal right to impose no-smoking policies in their rental properties without violating federal discrimination laws. However, it’s important to note that in 29 states and the District of Columbia, there are smoker protection laws that may offer some level of protection to smoking tenants, although these laws vary in their scope and application, and often do not directly impact housing policies. Therefore, while federal law largely supports landlords in restricting smoking in their properties, it’s crucial to be aware of and understand any specific state laws that might affect this issue by sourcing a legal professional.

Source: Multifamily Insiders

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

Listen On:

There is nothing worse than showing up to one of your units and seeing damage. Well, the only thing that might be worse is a tenant who believes they are not responsible for that damage and is calling it standard wear and tear.

We are using our personal stories to show you how we have combated this problem with our own properties and giving you some tips on how to set yourself AND your tenant up for success so that, hopefully, you won’t have to be bothered with this issue.

Give this episode a listen and learn how you can avoid this potential problem with your rental properties.

LINKS

👉 Episode 7: A Guide to Move Out Procedures and Security Deposits

👉 PDF: HUD Appendix 5C, TENANT DAMAGE versus “NORMAL WEAR AND TEAR”

👉 Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

👉 Help other DIY landlords discover what we have to say… Please leave us a review of our podcast!

On Apple Podcast or ITunes, please scroll to the bottom of our main page (with our logo) and click “Write a Review”.

On Spotify, please click the 5.0⭐ on our the front page of our podcast page.

👉 Join our Private Facebook Group! A space to ask questions and network with other DIY landlords.

👉 Follow us on Instagram

👉 Like us on Facebook

👉 Want the podcast link emailed to you weekly? Subscribe to our FREE newsletter, Landlord Weekly!

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

Check out samples of our newsletter👇 If you love it, you can subscribe from there!

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

With the college sports season’s thrilling climax, this is also an exciting time for real estate investors who own rentals in college towns that are being given a high profile. These landlords have likely long known that student rentals are one of the most lucrative places to make ongoing high yields.

Having the national spotlight focus on a college town where you invest is like having huge ads placed outside your property to attract future tenants. Colleges in the South and Midwest generally mirror real estate in those areas, which have provided some of the strongest cap rates for investors in recent years.

Here’s a closer look at the towns and cities where great sports teams pair with great investments. We ranked the college towns based on their rent-to-price (RTP) ratio. An RTP is calculated by dividing the gross monthly rent by the purchase price (or, in subsequent years, by the market value). A standard RTP that investors use is around 1%, often called the 1% rule, although an RTP above 0.6% is also considered good. Thus, if a property rents for $2,000/month and has a market value of $2,000, the RTP would be $2,000/$200,000, which is 1%.

It’s important to note that every market will have its fair share of ZIP codes with high and low RTPs. There’s cash flow to be made in every market—you just need to find it.

The Rent-to-Price Ratio of Each College Market

1. The University of Alabama (Tuscaloosa, Alabama): 0.76%

2. University of Dayton (Dayton, Ohio): 0.67%

3. Texas Tech (Lubbock, Texas): 0.66%

4. Northwestern (Chicago): 0.64%

5. University of South Carolina (Columbia, South Carolina): 0.64%

6. Indiana State (Terre Haute, Indiana): 0.63%

7. Texas A&M (College Station, Texas): 0.63%

8. Mississippi State (Starkville, Mississippi): 0.62%

9. University of Illinois (Champaign, Illinois): 0.62%

10. High Point University (Greensboro, North Carolina): 0.60%

Need a Lease Agreement?

A FREE account gets you access to over 200 free forms. Upgrade to a paid account (monthly, annually, or lifetime)

EZLandlord Forms Is Offering 15% 𝙊𝙛𝙛 For New Customers!

We cannot recommend these guys enough!

👉 State Specific Leases 👉 400 Forms to make your landlord-tenant relationship top notch 👉 200 FREE forms for those not ready to purchase 👉 4.8 Rating with over 5000 Reviews 👉 Pro Members get access to ALL leases and forms for $12 per month OR $75 if you purchase the annual membership 👉 YOU CAN BUY LIFETIME FORMS for $399

USE CODE 𝐒𝐓𝐀𝐂𝐈𝐄𝟏𝟓 to get 15% OFF ALL first-time purchases, EVEN THE LIFETIME FORMS!

A Closer Look at the Top College Towns

Tuscaloosa, Alabama

The University of Alabama is a big draw for real estate investors. However, the Alabama Crimson Tide isn’t the only reason to invest here.

Like other more northerly Alabama cities of Birmingham and Huntsville, Tuscaloosa County ticks the boxes for good investment criteria. It has low unemployment (2%), a population growing by 2% each year, a decent median income of $58,620, and a generally affordable median rent of $1,549 with a robust rental growth of 7%, which means investors can increase their cash flow each year. With a median home price of $205,030 and year-over-year price growth of 2%, Tuscaloosa is affordable, stable, and profitable.

According to the Tuscaloosa County Economic Development Authority, the main employers in the small city of 266,638 are the University of Alabama (6,839), Mercedes-Benz (4,500), and the DCH Regional Medical Center (3,444). Each long-established company is a stable source of employment.

Dayton, Ohio

Known as the birthplace of aviation, Dayton, Ohio’s real estate business takes flight thanks to its affordable median home price of $185,000, its 3% annual appreciation, reasonably affordable rent of $1,234, and main employer, the Wright-Patterson Air Force Base, with its workforce of 30,000 people. Other big employers in the area are Premier Health Partners (14,135) and Kettering Health Network (5,029). However, it ranks just below Tuscaloosa due to its 3% unemployment and stagnant population growth.

Lubbock, Texas

The 11th largest city in Texas, Lubbock enjoyed a stellar ranking in a 2023 survey of 500 college towns for Best Real Estate Investment Potential. That survey was echoed in BiggerPockets data, with a low 3% unemployment rate, a modest population increase (1%), a healthy median income of $59,228, an affordable median rent of $1,342, and an annual rent growth of 1%. Homes are also affordable, with a median price of $202,763, though price growth is stagnant.

Texas Tech is the biggest employer in the city. Various other employers contribute to diverse business infrastructure in manufacturing, agriculture, wholesale retail, and healthcare, including Covenant Health, United Supermarkets, Convergys, and Tyco Fire Protection Products.

However, Lubbock is more than a place to invest in real estate, which could be part of its charm. It was ranked No. 8 in 2022 for U.S. cities with the best work-life balance, No. 1 in 2023 for the best cities overall for recent college graduates, No. 6 (2022) for the best mid-size city business climate, and No. 10 (2022) for the best city for raising families.

Chicago, Illinois

Located 40 minutes outside Chicago in Evanston, Northwestern both benefits and suffers from being located in the metro area of a major city. Unemployment is at 4%. However, home appreciation is at 6%.

For investors, it’s interesting to note that the median income is $82,914, yet the median cost of a home is around $300,000—generally affordable by today’s standards. However, as major corporations move out of big Northeast cities to warmer states and remote work takes hold, Chicago has felt the hit with a few big defectors.

The Windy City has as experienced a small (-1%) population loss over the past year. Still, with established universities, hospitals, finance sectors, new tech businesses, and other attractions and businesses of a major city, along with relatively modest real estate prices compared to other major cities, Chicago remains a worthwhile real estate investment.

Final Thoughts

Successful college sports teams often come from successful universities, well embedded into the economic fabric of the vibrant city in which they reside, so it should come as no surprise that many of these cities also make for good real estate investments. It’s unsurprising to learn that many successful real estate investors started their journey as students, renting out rooms in a home they owned and building their empires from there. Whether you are an investor or want to kick-start your kids’ investing career, looking at cities with a successful college sports team will steer you in the right direction.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

The media tends to side with tenants and take a negative view of landlords overall. One notable exception was an episode of HBO’s Silicon Valley, where the hapless Jared has tried for over a year to evict a nonpaying “professional tenant” who is currently subleasing Jared’s unit through Airbnb because California’s landlord/tenant laws are so biased in favor of the tenant that an eviction can take close to an eternity.

At the same time, Erlich (who rents the rooms in his home to Jared and the other characters trying to build the fictional tech company Pied Piper) is demanding one of his tenants and soon-to-be-supervillain Jian Yang leave his house (video contains NSFW language) and unfortunately lets Jared’s situation slip. This inspires Jian Yang to decide that instead of leaving, as Erlich requested, he would instead stay and simply stop paying rent.

While that episode was quite amusing, some municipalities seem to be trying to transcend parody into something beyond satire. New York, for example, just arrested a woman for changing the locks on a squatter in the $1 million home she inherited.

According to a New York Post story about the incident:

“[Adele] Andaloro claims the ordeal erupted when she started the process of trying to sell the home last month but realized squatters had moved in—and brazenly replaced the entire front door and locks.

“She said she got fed up and went to her family’s home on 160th Street—with the local TV outlet in tow—on Feb. 29 and called a locksmith to change the locks for her.”

Understandable, but not a wise course of action. The two got into a heated argument, and the police were eventually called. As the New York Post article notes, “Under the law, it is illegal for the homeowner to change the locks, turn off the utilities, or remove the belongings of the ‘tenants’ from the property.” The word “tenant” is an extraordinarily generous euphemism in this case.

What complicates matters more is that in New York City, someone can claim “squatters rights” after being in a home for just 30 days. But “’[b]y the time someone does their investigation, their work, and their job, it will be over 30 days and this man will still be in my home,’ Andaloro said.” So, that left Andaloro between a rock and a hard place:

“Andaloro was ultimately given an unlawful eviction charge because she had changed the locks and hadn’t provided a new key to the person staying there, the NYPD confirmed to The Post. She was slapped with a criminal court summons, cops added.”

This case may be exceptional, but it is by no means unique. Also, in New York, a couple bought a $2 million “dream home” to care for their son with disabilities but couldn’t move in because a squatter had beat them to it. In another home, a squatter completely destroyed a property in the Rockaways, where dozens of emaciated dogs and cats were trapped inside on the verge of death.

The New York Post quotes one attorney saying such cases have increased “40% to 50% in similar cases in the wake of COVID.”

This is made all the more frustrating by New York’s apparent lack of interest in prosecuting normal crimes. In 2022 and 2023, over half of felonies were downgraded to misdemeanors and misdemeanor cases resulting in a conviction plummeted from 53% in 2019 to 29% in 2022.

Meanwhile, New York’s crime rate skyrocketed in 2022.

Fortunately, crime has ebbed a bit in New York City (and the rest of the country in 2023 and so far into 2024). But I feel pretty confident in saying it’s not because people like Adele Andaloro are being arrested.

I should also note that this isn’t just a problem in New York. On the other side of the country, in Oregon, an investor posting as a squatter explained on X (formerly Twitter) how he could “steal a property” due to Portland’s laws on the subject.

Indeed, I would have thought such problems would be more acute in California, which has the second-highest homeless rate in the country. Unfortunately, California chose a “housing first” policy instead of a “shelter first” policy to help homeless people get off the street. Providing housing for each homeless person is, not surprisingly, extremely expensive, especially in high-priced places such as Los Angeles and San Francisco.

Getting back to New York: Despite this absurd story, the city has done a mostly good job with its homeless population and has been able to shelter 96% of its homeless population, whereas California shelters a paltry 38%. While some of this may be due to the more temperate weather in most of California as compared to New York, the fact that three times as many homeless people died in Los Angeles as in New York City in 2020-2021 (1,988 to 640) shows that it’s not all that.

Looking for more information or a support network on the investing side of rental properties?

Check out BiggerPockets! They provide resources and tools to help people learn about real estate investing and build wealth through rental properties. Their website offers a community of over 2 million members, educational content, networking capabilities, and software tools. BiggerPockets also publishes books and podcasts about real estate investing.

The Erosion of Property Rights

The story of Adele Andaloro really shows less about how municipalities choose to help their homeless population and more about the erosion of property rights in many places throughout the United States. We’ve seen this in the deluge of passed and proposed legislation targeting property owners throughout the country.

Now, I should note that Andaloro made a huge mistake. As indefensible as her situation was, she should not have taken the law into her own hands, especially in a state as unfriendly to landlords as New York.

I should also note that landlords have more leverage in economic transactions than tenants do, and so the law does need to protect tenants. Landlords, after all, are the ones who write the leases. So, it’s incumbent upon the government to make sure the landlord cannot put any overly arduous or unfair clauses in that lease.

Laws that require properties to be maintained or 24-hour notice to be given to a resident before entry or mandating evictions go through the court system and not be done with hired muscle are all legitimate and necessary in any functional and just society. But these “rights” have clearly gone way too far in many municipalities. For example, Denver just passed a law preventing landlords from demanding a tenant leave for any reason other than “just cause,” i.e., “nonpayment of rent, violation of lease terms, nuisance, and engaging in illegal activities.”

This means if a property owner ever intends to sell their house, move into it, or give it to their kids, they are simply out of luck. (Other states and cities have passed laws requiring landlords to offer extended notice and pay moving costs in such cases, which I actually think is reasonable.)

Regarding so-called squatters rights, legally speaking, they are supposed to simply be that “[a]n individual may claim rights as a squatter if they are roommates, tenants, or occupying property that is abandoned or not used.” This is just adverse possession, a somewhat odd law that transfers property from the owner to its occupant if the occupant has continuously occupied the property for a certain length of time without refraining from the owner. States vary from three years (Arizona) to 30 (New Jersey) on just how long that needs to be.

But in many cases, squatting has become synonymous with trespassing. And instead of punishing the perpetrator, the victim is the one who must stomach the cost.

In Missouri, where we do most of our investing, “just like most other states, [Missouri] doesn’t have special laws regarding squatters’ removal. Therefore, to evict a squatter, you’ll need to go through the state’s eviction process.” This means for the offense of having someone break into our property, we have to pay to evict them and lose out on the opportunity cost of any rental income that could come in during that time.

This is the case in most states, so the big question to investors is, how friendly are the landlord/tenant laws where you invest? Because if you do get a squatter, the question becomes how hard it will be to evict them. Indeed, I had gotten several, and while the courts here are rather slow, they are thankfully much faster than in New York.

(In some areas, it is also sometimes worth boarding the windows and doors, at least during renovation, to prevent a squatter from getting in.)

SparkRental.com did a study and came up with a list of the most renter-friendly and landlord-friendly states. It looked like this:

Back in 2020, BiggerPockets also did an analysis with similar results. It found the five most landlord-friendly states to be:

- West Virginia

- Arkansas

- Louisiana

- North Carolina

- Alabama

And the five most tenant-friendly (or perhaps most antagonistic to landlords) were:

- Vermont

- Delaware

- Rhode Island

- Maine

- South Dakota

Moving Forward

While cases like Adele Andaloro make the headlines, overall, they are still rather rare. You don’t want to become paranoid.

Still, in a time when such farcical cases are becoming more commonplace, and property owners are under continued legislative attack, it’s important to know which places are the most amenable to property ownership. This is especially true for buy-and-hold investors.

Indeed, in the least landlord-friendly places (New York being one of them), I would probably lean away from investing in buy-and-hold residential real estate there. (Commercial, fortunately, doesn’t have these problems.)

In other cities and states that are still tough on landlords but below the farce, I would still recommend caution. Budget for higher administrative and legal costs and a higher economic vacancy factor. And make sure any potential acquisition still works with such restraints.

Finally, make sure to understand your local laws, and no matter how ridiculous they may be, don’t take the law into your own hands.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

The automation of rental property management has revolutionized how landlords operate, streamlining tasks and enhancing efficiency beyond measure. From showcasing vacancies to collecting rent, landlords are automating nearly every aspect of their business, saving time and resources while improving tenants’ experiences.

In the digital age, there’s simply no going back once tech has advanced. A modern touring and renting procedure makes all the difference to today’s tenants, and we may be heading into a renters’ market. To combat this, landlords can identify where antiquated practices are replaceable with tested tech.

The United States Census Bureau asserts that the national rental vacancy rate has reached 6.6%. This is a 13.8% increase from the average vacancy rate in 2022

1 Garnering Interest with Virtual Tours

Virtual tour software showcases available units online, giving an elevated remote experience for inquiring tenants. People are doing more research than ever and are more likely to schedule an in-person tour after a virtual tour than with a listing that leaves them with questions. This saves time for both parties and widens the property’s reach beyond geographical limitations – a huge plus for potential renters moving a plane ride away.

2 Simplifying and Screening Tenant Applications

Digital application collection allows applicants to submit documents and information electronically. Integrated background check tools streamline the selection process and ensure a thorough assessment.

With AAOA’s own tenant screening app, applicants can also pay a screening fee, and landlords receive notifications immediately to view completed credit and background checks.

Tenants that are less tech-savvy or new to renting often fail to satisfy these requirements prior to in-person tours. While landlords prefer to hold firm, sometimes a gut feeling or an extended vacancy leads to letting their guard down. For that reason, this solution is very effective in tandem with tour-scheduling software, as it brings these requirements to their immediate attention and bars them from skirting this step before touring.

3 Streamlining Property Tours

The most time-consuming part of filling vacancies, and arguably the most difficult for landlords, is the scheduling and execution of in-person tours. It takes time to line up the availability of all parties, travel to the property and run the tour – all while running the risk that the potential tenant arrives late, doesn’t arrive at all, or fails to meet rental requirements after the fact.

Self Tour technology, like InstaShow, advertises listings and allows renters to tour the property after they have passed background checks and submitted all the necessary documentation. This software eliminates the need to arrange a mutually available meeting time and gives renters the freedom and flexibility to tour vacancies when it is convenient.

This alleviates countless pain points for renters, such as typical stop-start communication around scheduling, juggling work and personal schedules, and organizing background checks and application data on one platform.

Once a user has their profile verified, they can schedule tours via the app within the listing’s parameters, notifying property managers immediately. The software then facilitates a secure and seamless experience with real-time identity verification before using Bluetooth technology to allow access to the property.

The software tracks their experience as they walk through the unit and for added security, can pair with smart cameras to enable real time surveillance and 2-way communication.

Looking for the next level of landlord software before handing off to a property manager?

Hemlane is a software that is built to grow with your needs as a landlord.

For a minimal amount, there’s a really good basic package but what we love is the option to upgrade and add 24/7 maintenance management on.

Hemlane offers complete financial support as well. You can link multiple bank accounts for direct deposit rent payments, add automatic late fees, sends reminder notifications to your tenants, and has a detailed profit and loss statement that can includes automatic and manual uploads of income and expenses.

It gets better! If you reach a place where you are ready to hand off management to a property manager, Hemlane has that too under their “Complete” option.

You can try Hemlane out FREE for 14 days (no credit card required) to see if its a good fit for you!

4 Automating Lease Signing

Digital lease agreements can be signed and stored securely online. This eliminates the hassle of printing, canning, mailing, and maintaining documents, making it convenient for both landlords and tenants. Most property management platforms charge for this feature, while others, like Innago, offer it for free.

5 Facilitating Rent Collection

Online portals or apps for rent collection automate monthly payments, ensuring timely and consistent transactions. Tenants can set up automatic payments, reducing the risk of late or missed payments. Landlords can track payment histories, send reminders, and generate reports effortlessly.

6 Enhanced Communication and Maintenance Requests

Integrated communication tools maintain consistent and transparent communication with tenants. Automated messages for rent reminders, lease renewals, or general announcements can be scheduled, fostering a proactive and professional relationship. This can include centralizing maintenance requests, thereby allowing tenants to submit issues for review. Landlords can track these requests, assign tasks to maintenance staff or contractors, and monitor the status of repairs, ensuring timely resolution and tenant satisfaction.

CONCLUSION

Modernizing the rental property management process offers landlords unparalleled efficiency, convenience, and organization. To harmoniously transition into using these kinds of software, finding platforms that offer many solutions in one place is ideal. However, the all-in-one platforms are by far the most expensive. Therefore, it may be optimal to consider one platform to streamline advertising listings and facilitating tours, and another, like Doorspot, that begins with signing the lease and encompasses ongoing communication for just $54/month.

Embracing these technological advancements automates the rental process, improves tenant satisfaction and ultimately contributes to a more successful and profitable business.

LEAH MAHER

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

Listen On:

So, the one thing that everyone needs to realize is that how we own and operate OUR rental property business may differ from YOUR way of doing things. I know, crazy, right?

The thing is that the kind of rental that you prefer, be it single family home or large multifamily complexes and the location of those, be it out of state or right in your backyard, and the condition of those, be it run down with a ton of added value or with everything in place so all you have to do is step in and run it…all makes a huge difference on what your expenses will be.

HOWEVER, there are a bunch of expenses that some landlords, us included, might forget to consider when evaluating a new property or maybe even when making a change to an existing one.

Those hidden expenses are what this episode is all about. Give it a listen to learn what you might have to prepare for.

LINKS

👉 Episode 20: Part 1: The Nuts and Bolts of Residential Rental Property Insurance

👉 Episode 21: Rental Property Insurance Part 2, Interview with Ryan Bravo

👉 Episode 28: The Cash Reserves Blueprint: Protecting & Expanding Your Portfolio

👉 Episode 39: 50+ Must Ask Questions When Hiring a Property Manager, Part 1

👉 Episode 40: 50+ Must Ask Questions When Hiring a Property Manager, Part 2

👉 Purchase our 14-page Property Management Questionnaire to use when interviewing or vetting a new property manager.

👉 Your Landlord Resource: All of our Free Downloads (Email Templates, Guides, PDF’s)

👉 NOLO Legal Forms: Make your business an LLC

Structuring your business as an LLC can bring important advantages: It lets you limit your personal liability for business debts and simplify your taxes. Here, you’ll find the key legal forms you need to create a single-member or multi-member LLC in your state, including:

• LLC articles of organization

• operating agreement for member-managed LLC

• operating agreement for manager-managed LLC

• LLC reservation of name letter, and

• minutes of meeting form.

Form Your Own Limited Liability Company has easy-to-understand instructions, including how to create an operating agreement that covers how profits and losses are divided and major business decisions are made. You’ll also learn how to choose a unique LLC name that meets state legal requirements and how to take care of ongoing legal and tax paperwork.

Launch Your LLC Today!

👉 Wool Dryer Balls (Tenant Gift)

👉 PDF for the cardstock note we left with the dryer ball gift.

👉 Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

👉 Help other DIY landlords discover what we have to say… Please leave us a review of our podcast!

On Apple Podcast or ITunes, please scroll to the bottom of our main page (with our logo) and click “Write a Review”.

On Spotify, please click the 5.0⭐ on our the front page of our podcast page.

👉 Join our Private Facebook Group! A space to ask questions and network with other DIY landlords.

👉 Follow us on Instagram

👉 Like us on Facebook

👉 Want the podcast link emailed to you weekly? Subscribe to our FREE newsletter, Landlord Weekly!

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

Check out samples of our newsletter👇 If you love it, you can subscribe from there!

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

By Deirdre Mundorf

Know your rights as a tenant—and limitations as a landlord. While landlords hold a lot of power, there are several things they are not legally allowed to do.

Whether you are looking to rent an apartment or considering buying a rental property, it is essential to know what landlords are and are not allowed to do. Just as landlord rights protect landlords, tenants also have rights. Understanding what a landlord cannot do will protect you from being treated unfairly as a tenant and prevent you from crossing a legal line when renting a property. Read on to learn more about some of the laws that landlords must follow when renting their property. Keep in mind that landlord tenant law provisions can vary by state, so before renting to or from someone, read up on the local landlord and tenant laws in your state.

1. Use Discriminatory Practices

{kind=link}

Photo: istockphoto.com

While landlords may choose to use a tenant screening service, they may not use discrimination as the basis of any decisions regarding current or potential tenants. The Fair Housing Act states that any form of discrimination based on race, disability, color, religion, national origin, gender, sexual orientation, or familial status is illegal. If you feel like your landlord or potential landlord is using discriminatory practices, file a complaint on the HUD website or contact a local advocate in your state.

2. Enter the Property Without Giving Sufficient Notice

{kind=link}

Photo: istockphoto.com

A landlord may own the property, but that does not mean that they are able to enter it any time they wish. Most states have laws in place requiring landlords to provide their tenants with a minimum of 24 hours notice before they enter the property. In some states, they are required to provide written—not even via text or email—notice unless the tenant has agreed to the latter form of communication. Furthermore, landlords may only be allowed to enter a property (after providing sufficient notice) during regular business hours—9 a.m. to 5 p.m., Monday through Friday. Exceptions to this rule include emergencies or if the landlord suspects that the tenant has moved out and left the rental abandoned.

If your landlord has not been providing sufficient notice before entering your rental unit, start by making sure they are aware of the law. If this does not change their behavior, you can report them to the local housing office or even contact the police to file trespassing charges.

3. Evict Tenants Without Following Legal Guidelines

{kind=link}

Photo: istockphoto.com

Landlords have the right to evict tenants. However, there are limits to that right and a landlord is required to follow the proper procedures mandated by their state. In some states, they are required to give 30 days notice (or even more in some places), while other states do not require much, if any, notice to be given to the tenants before eviction can occur. If a landlord evicts a tenant without following their state’s procedures, it is possible that they could face burglary or trespassing charges. Contact your local housing authority immediately if you think your landlord evicted you without following the proper channels.

4. Raise the Rent in the Middle of the Lease Without Justifiable Cause

{kind=link}

Photo: istockphoto.com

Even though most landlords are renting property for income, they are not allowed to simply raise the rent in the middle of the lease to make more money. When you and your landlord signed the lease, you both agreed to the stated rent payments. Unless they have just cause—such as a roommate moving into the property or a new pet joining the household—they cannot simply decide to raise the rent before the lease is up.

5. Deny Requests for Repairs Related to Health or Safety

{kind=link}

Photo: istockphoto.com

While a landlord is not obligated to complete all requested repairs, they are also not allowed to refuse to complete repairs that are necessary for the health or safety of their tenants. If the property has mold, broken utilities, or other serious issues, the landlord will have to address them promptly. If you do not feel like your landlord is taking a concerning issue seriously, seek guidance from your local housing office.

Your Landlord Resource has teamed up with Toggle, a division of Farmers Insurance that offers competitive pricing of renters insurance for tenants.

Policies can start as low as $5 a month!

Copy and share our link with your tenants to get them started: http://go.gettoggle.com/SH1E Download this PDF to present to your tenants with your renters insurance request! Toggle Renters Insurance Flier.pdf

6. Rent a Room Without a Window

{kind=link}

Photo: istockphoto.com

If you’re considering living with private owners renting a room out, know that one of the rules for renting is that bedrooms must have a window or exterior door. In fact, it is illegal for anyone to rent a room that does not have a window. In order to qualify as a “bedroom” suitable for sleeping, a room must have an egress window or door that will allow the occupant to safely escape in the event of a fire. Homeowners are not allowed to rent out certain parts of their property, and this most certainly includes windowless rooms.

7. Charge Unreasonable Late Fees

{kind=link}

Photo: istockphoto.com

Late rent payments happen, and landlords are allowed to charge late fees. However, while landlord leasing requirements can vary by state, many include limitations on the fees that can be charged for late rental payments and may also specify a grace period for late payments. For example, states such as Maryland, New York, Delaware, Nevada, North Carolina, and Oregon only allow late fees up to 5 percent of the monthly rent. However, several states have no stated limit on the maximum late fee. If you live in one of these states—including Connecticut, Florida, California, Indiana, Colorado, and Louisiana—read your lease closely and do your best to make sure that you are on time with your rent payments to avoid being charged extra.

8. Withhold the Security Deposit Unjustly

{kind=link}

Photo: istockphoto.com

It is unlikely that you’ll find any landlords who do not require a security deposit. The security deposit is designed to protect landlords for both private owner house rentals and larger apartment complexes against damage that tenants cause to the property. Once the tenants move out, landlords can withhold some or all of the security deposit to cover necessary repairs, such as fixing something that was broken by the tenant. What they cannot do is withhold the security deposit to cover normal wear and tear, such as slightly worn carpet or a few scuff marks on the walls or floors.

9. Charge Pet Fees or Deny Housing for Individuals with Service Animals

{kind=link}

Photo: istockphoto.com

Landlords are not required to allow pets in their properties. And, if they decide that they are going to allow individuals with a cat or dog to live in their house, they have the right to charge a pet fee or an additional monthly rent payment. The exception to this, however, is for individuals who have a service animal. According to the U.S. Department of Housing and Urban Development, in nearly all cases, landlords cannot deny housing or refuse to accommodate an individual’s need for a service animal.

10. Raise the Rent in Retaliation of Something the Tenant Did

{kind=link}

Photo: istockphoto.com

If a landlord raises your rent after you made a complaint against them, they are likely breaking state law and the landlord tenant act. These laws are designed to protect tenants against retaliation after taking a legal action against their landlord, such as complaining about unsafe living conditions, following state laws to withhold some or all of the rent for uninhabitable conditions, or coordinating with other tenants to voice your views. Take action if you believe your landlord is raising your rent out of retaliation for something you did. Consider filing a suit in your local small claims court or making a complaint against your landlord to your local housing department.

FAQ About What a Landlord Cannot Do

Learn more about some of the limitations to the power a landlord holds by reading through the frequently asked questions below.

Q. Can a landlord raise rent during a pandemic?

Unless the city or state has put a rent freeze into effect because of the pandemic, landlords are allowed to raise rent.

Q. Can a landlord come on the property without notice?

No, in most states, landlords are required to give sufficient notice (typically 24 hours) before entering a tenant’s property.

Q. Do I need to have landlord insurance if I rent properties?

Landlord insurance is not required when renting a property. However, you may decide that the additional coverage provided by landlord insurance is worth the additional cost.

Q. Can a landlord kick me out?

Landlords have the right to evict tenants who do not follow the agreements set in the lease. However, in most states, they are required to give proper notice before executing an eviction.

Q. Do landlords forbid tenants to bring in animals?

Yes, with the exception of service animals, a landlord has the right to forbid their tenants from having animals in their rental unit.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

2023 was a volatile year for the multifamily industry.

Demand patterns and rent prices returned to a post-pandemic normal, but apartment communities’ operating expenses skyrocketed while nationwide occupancy rates declined.

Additionally, the supply of new units entering the marketplace drove up competition and gave renters more control in choosing where to rent.

Those issues are setting the stage as the industry turns the calendar. How will they impact your communities’ plans to attract, attain and retain residents? Let’s look deeper at the challenges owners and operators face in 2024 and how to overcome them.

Challenge #1: 2024 will be another record-breaking year of new unit deliveries.

According to Yardi Matrix, an additional 500,000+ new units will enter the marketplace in 2024, giving renters the upper hand by having more apartment choices than ever and undeniably impacting your existing communities’ ability to attract new residents.

Solution: Ensure your apartment’s digital marketing presence remains competitive by letting renters see the inside of your units.

The opening of a new apartment community nearby is less threatening when your apartments’ digital marketing presence prioritizes the needs of prospective renters. You’ll stand out in 2024 (and beyond) and make it easier for renters to choose your community when you make it possible for every renter to see the inside of the specific floorplan or unit they’re interested in on your apartment’s website and other online channels.

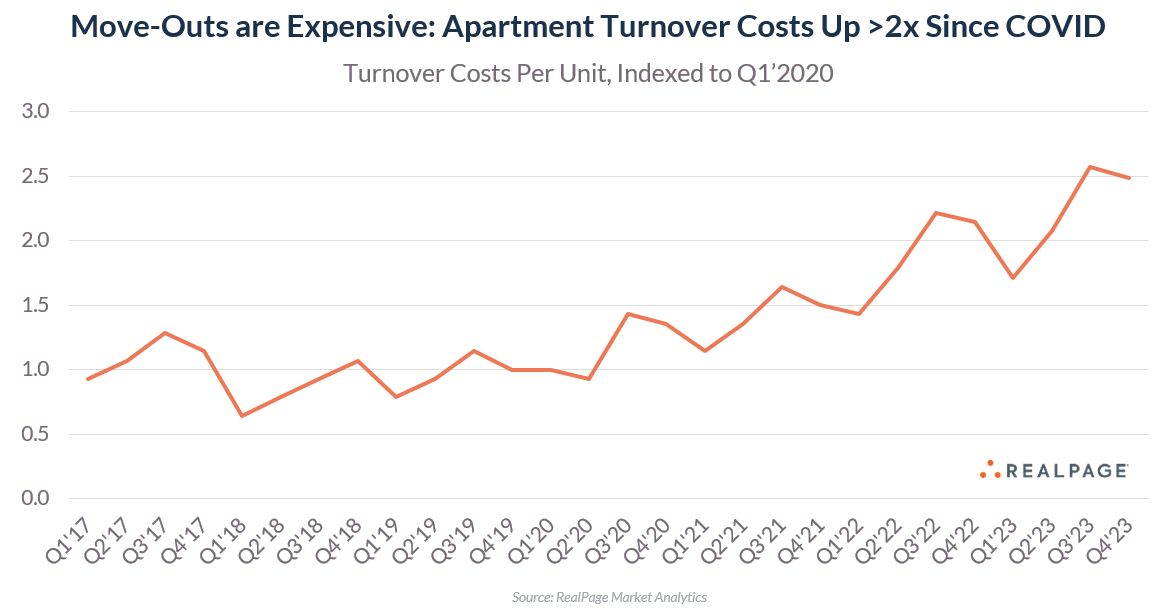

Challenge #2: Turnover costs are on the rise in 2024.

According to Jay Parsons, rental housing economist at RealPage, turnover costs have more than doubled since the COVID pandemic hit and can “easily exceed one month’s rent” of that unit. Alarmingly, the rising costs do not factor in marketing expenses or vacancy loss.

Solution: Make resident retention a priority by focusing on your renewal strategy.

Your lease renewal strategies in 2024 will be critical as you combat rising operational expenses. Treat renewal pricing as crucially as you would for a new lease and include any concessions, if necessary, such as offering renewal rates below what the current resident is paying.

Additionally, you must provide an excellent resident experience, as that, above anything else, is the best method for ensuring more residents choose to stay.

Looking for the next level of landlord software before handing off to a property manager?

Hemlane is a software that is built to grow with your needs as a landlord.

For a minimal amount, there’s a really good basic package but what we love is the option to upgrade and add 24/7 maintenance management on.

Hemlane offers complete financial support as well. You can link multiple bank accounts for direct deposit rent payments, add automatic late fees, sends reminder notifications to your tenants, and has a detailed profit and loss statement that can includes automatic and manual uploads of income and expenses.

It gets better! If you reach a place where you are ready to hand off management to a property manager, Hemlane has that too under their “Complete” option.

You can try Hemlane out FREE for 14 days (no credit card required) to see if it’s a good fit for you!

Challenge #3: Apartment marketers must generate leads with smaller budgets in 2024.

Many are responding to the increasing expenses of owning and operating a multifamily property by tightening their budgets, which sometimes include marketing and advertising. The fear is that reducing marketing investment could also reduce lead counts.

Solution: Develop the right mix of marketing channels for producing better-qualified leads.

Even though it may feel that you need more marketing tools and higher budgets these days to manage multiple channels, the truth remains that there’s a very typical pattern by which renters discover, engage, and eventually select an apartment. We call it the “Leasing Funnel,” or the mix of apartment marketing channels you can apply that puts your community front and center throughout a prospect’s search.

Following the Leasing Funnel as you establish your multifamily marketing plan for 2024 will make your marketing expenses more efficient and help prospects discover and learn essential information about your community online and feel more comfortable with making the life-impacting choice of where to rent an apartment.

Takeaways

- New Unit Boom: 2024 will see a record influx of new apartments, increasing competition and requiring stronger digital marketing with floorplan-specific visual content showcasing the inside of your units to stand out.

- Rising Turnover Costs: Combat skyrocketing turnover costs by prioritizing resident retention through competitive renewal rates and an excellent resident experience.

- Smaller Marketing Budgets: Optimize marketing efforts with the “Leasing Funnel” strategy, focusing on the right mix of channels to attract better-qualified leads while maximizing efficiency and return on investment.

Source: RentVision

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

By Krista Reuther

Are you new to the world of renting? Are you a landlord looking to diversify your portfolio? Or are you just curious about mid-term rentals?

No matter why you’re here, we’re glad you found us! We’ve put together this guide as an overview of everything you need to know about medium-term rentals.

In this blog, we’ll cover everything from what a mid-term rental is, how to go about their lease agreements, and who uses them. We’ll also talk about the pros and cons of managing mid-term rentals. Let’s dive in!

Table of Contents

- What Is a Mid-Term Rental?

- Who Uses Mid-Term Rentals?

- What You Need in a Mid-Term Lease Agreement

- What Are the Pros of Managing a Mid-Term Rental?

- What Are the Cons of Managing a Mid-term Rental?

- Conclusion

What Is a Mid-Term Rental?

You’ve probably heard of short-term and long-term rentals, but what exactly is a mid-term (or medium-term) rental? The answer is in the name: a mid-term lease agreement is a rental agreement between a property owner and tenant that lasts for less than one year but usually more than one month.

Ordinarily, short-term rentals last for less than one month (and are sometimes referred to as vacation rentals), while long-term rentals are typically year-long leases. Medium-term rentals fall into that sweet spot of at least one month but average three to nine months.

Mid-term rentals are ideal for landlords in highly populated cities or college towns. In addition to populous metropolises, medium-term rentals work well in areas where seasonal work is common, such as near agricultural centers. They’re also great for prospective landlords who want to get into the rental market but aren’t ready to have a long-term commitment.

Who Uses Mid-Term Rentals?

If you’re pursuing real estate investing, it makes sense that you’d want to maximize your return on investment. Mid-term rentals can offer a surprising return on investment despite frequent turnover. Mid-term rental demand is growing, especially with the post-pandemic rise in remote work creating the profile of a “digital nomad”. And of course, prolonged business trips and vacations will always create demand for flexible lease durations.

Let’s take a look at some of the most common groups of people that use mid-term rentals:

- Traveling nurses: At the height of the pandemic, traveling nurses needed housing like never before, and they’re still in high demand across the country. Rather than shell out exorbitant fees to live in a trendy Airbnb, mid-term rentals allowed nurses to establish a home away from home.

- Students: Students often need somewhere to stay while they attend class. Mid-term rentals provide students with an affordable option that doesn’t require them to live on campus or commute long distances daily.

- Digital nomads: Digital nomads are people who work from home or remotely and travel frequently as a lifestyle choice. They tend to be more transient than other travelers —they may stay with friends or family before finding a new location where they can settle down for a while.

- Business professionals: Many industries require their employees to travel. Some companies host workers in mid-term corporate housing; others seek their own mid-term housing solutions.

Other tenants who may use medium-term rentals include families relocating to a new city and professionals heading to a new place to start an internship. While all these groups may have different reasons for moving, they generally use mid-term rentals because they have reasonably extended short-term housing needs.

A landlords one stop shop for tenant management…for FREE

You can’t beat free and the only time you pay is if you want to purchase a lease or have expedited rent deposits. Most everything else costs zip, zero, zilch.

What You Need in a Mid-Term Lease Agreement

Mid-term rentals are unique in many ways, which means you’ll need to make sure your lease agreement reflects your specific rental. There are several things to consider when drafting a mid-term lease agreement, including but not limited to:

- The length of stay/occupancy (rental period of one to 12 months)

- The amount of rent

- Security deposit and other applicable fees

- Amenities – utilities like Wi-Fi access and whether the rental house is furnished or not

- Local landlord-tenant laws and regulations

- Tenants’ rights

- The responsibilities of both the tenant and landlord

Generally, medium-term lease agreements may not involve a lot of legal stipulations like traditional leases. However, check your local landlord-tenant laws to make sure you’re abiding by any specific term-based lease requirements. We also recommend that you chat with your attorney or local housing authority before any documents are signed to ensure you’re doing everything by the book.

What Are the Pros of Managing a Mid-Term Rental?

While long-term rentals can be great for owners looking for a steady rental income stream over several years, mid-term rentals offer unique advantages, including:

- You have access to new tenants who may be more willing to work with you and are less likely to default on their lease agreement than long-term tenants who have lived there for several years.

- Unlike short-term housing, you’ll have a more steady cash flow that is less susceptible to seasonal fluctuations.

- You have more flexibility since you don’t have to worry about a long-term commitment.

- Your business is likely to flourish over time if the demand for medium-term rental units continues to grow.

What Are the Cons of Managing a Mid-term Rental?

As with any business venture, there are certain aspects you need to be aware of if you’re going to be handling a mid-term rental, such as:

- Your property is more likely to be used for unethical activities. This is true of short-term and mid-term tenants but is slightly more common with short-term renters because they don’t plan on being there for very long and aren’t as invested in their community or neighborhood. If something unethical happens on your rental properties, it could lead to other issues like vandalism or noise complaints. To combat this, make sure your lease agreement clearly defines acceptable and unacceptable uses of the property, and be sure to screen your tenants thoroughly.

- If you don’t have experience managing mid-term rentals, it can be challenging to find the best tenants. However, there are digital tools you can use to market your listings efficiently. Make sure your rental application is easy to fill-out and professional to attract great tenants.

- There can be more legal issues in managing a mid-term rental than a short-term one. That’s why it’s so important to speak with your attorney or local housing authority before a lease is signed. You need to know the full scope of potential risks to determine if you want mid-term rentals to comprise a share of your real estate investing efforts.

Conclusion

Mid-term rentals offer fantastic opportunities for prospective landlords and seasoned property managers alike. With a wealth of prospective tenants and the flexibility of a shorter commitment, this type of lease can prove to be lucrative. Mid-term rentals are an interesting and exciting way to diversify your investment portfolio, just remember to speak with an attorney or housing authority to confirm mid-term landlord expectations.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇