Listen On:

You know the neighborhood when you buy. But do you really know it now that you own and manage the property?

In this Shorty episode of the Your Landlord Resource Podcast, Kevin and Stacie take a topic they first introduced in Episode 23 and go deeper — moving beyond marketing copy to explore what it truly means to understand the neighborhood surrounding your rental property.

From discovery walks and walk scores to fair housing guardrails and tenant retention, this conversation is packed with practical insights that help self-managing landlords become more confident, more informed, and more competitive in their local rental market.

WHAT YOU’LL LEARN IN THIS EPISODE

- Why tenants rent a lifestyle — not just a unit — and how knowing your neighborhood helps you speak to that

- How neighborhood knowledge gives you a competitive edge during showings without following people around

- What to say (and what never to say) when a prospective tenant asks “What’s the neighborhood like?” — and why fair housing certification matters

- The discovery walk habit and why doing it at different times of day reveals an entirely different neighborhood

- The Sacramento midtown story: what a late-night walk taught Kevin and Stacie about their own rental area

- Walk Score, Bike Score, and the EPA National Walkability Index — free tools and their limitations

- The six neighborhood categories every landlord should know: walkability, entertainment and leisure, schools and family amenities, transportation and parking, major employers, and safety indicators

- Why co-working proximity has become a genuine amenity in the hybrid work era

- How neighborhood awareness sharpens your rent pricing decisions

- Using neighborhood knowledge during tenant onboarding and move-in — not just at showings

- Why being a plugged-in landlord builds long-term tenant retention

- Practical tactics: how to actually do the research, from local social media to Chamber of Commerce connections

LINKS & REFERENCES MENTIONED IN THIS EPISODE

Episode 23 – Tips On Marketing Your Rental Property, Part 1

Read our Blog: Know Your Rental Neighborhood

EPA National Walkability Index

SpotCrime – Public Crime Data

Fair Housing Institute – Certification Courses (Use Code: YLR26 for 20% off first order)

Connect with Us:

🌎 Visit our website

📧 Subscribe to our newsletter.

👆Click this LINK to select from our FREE Landlord Forms and Doc’s

🤳Text Us SMS text to 650-489-4447. We love questions and love letters, hate mail not so much!

📩Email us at: [email protected], [email protected]

✔️Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

📱 Follow us on Instagram, Facebook, & join our private Facebook group

🎧 Listen & Subscribe on Apple Podcasts, Spotify, or your favorite podcast app

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

Estimated reading time: 3 minutes

Provided by The Fair Housing Institute

As the demand for housing continues to rise, property managers face the dual responsibility of maintaining occupancy standards and adhering to fair housing regulations. Occupancy limits are a fundamental tool used to ensure the safety, comfort, and well-being of residents while safeguarding property integrity. However, enforcing these limits while remaining compliant with fair housing laws can present challenges, particularly when requests for reasonable accommodation are involved.

This article explores the critical role of occupancy limits, the legal framework governing their enforcement, and the considerations property managers must account for when handling requests for exceptions.

The Importance of Occupancy Limits

Occupancy limits are established to maintain safety standards and prevent overcrowding in rental units. These limits are typically based on state and local housing codes, which take into account factors such as the square footage of a unit, the availability of exits, and the capacity of essential systems such as plumbing and ventilation. But what does enforcing these types of limits ensure for properties?

Enforcing occupancy limits is essential for ensuring safety compliance, as overcrowded units can pose significant risks, including increased fire hazards, restricted emergency access, and excessive strain on the property’s infrastructure. Additionally, occupancy limits help maintain the quality of life for all residents by minimizing noise, preventing property damage, and reducing wear and tear on shared amenities. Lastly, adhering to legal guidelines for occupancy limits not only helps preserve the well-being of the community but also shields property owners and managers from potential legal disputes and costly penalties.

While occupancy limits are essential for these reasons, property managers must enforce them in a manner that also aligns with federal fair housing laws.

Enforcing Occupancy Limits: Key Considerations

When enforcing occupancy limits, property managers must approach the task with professionalism and an understanding of both their legal obligations and the rights of residents under fair housing regulations. The following considerations will help guide enforcement in a fair and compliant manner:

1. Can Occupancy Limits Be Enforced?

Yes, property managers are within their rights to enforce occupancy limits, as long as these limits are clearly defined in the lease agreement and compliant with state and local regulations. However, it is important to recognize that exceptions may arise in the context of fair housing laws. For example, residents may request reasonable accommodations that necessitate a deviation from the set occupancy limits.

2. How Should Suspected Violations Be Addressed?

When a property manager suspects that a unit is housing more occupants than allowed, the first step is to confirm the facts. This involves engaging with the residents to discuss the terms of the lease and the occupancy policy. Should a violation be confirmed, it is necessary to proceed with addressing the issue as a lease violation. However, property managers must remain open to the possibility that a request for reasonable accommodation may alter the course of action.

3. What Practices Should Be Avoided?

To avoid potential fair housing violations, property managers should refrain from inquiring about the composition of the household in terms of familial status (i.e., whether there are children in the home). The focus should remain on the number of individuals residing in the unit, as family status is a protected category under fair housing law. Unless your occupancy policy explicitly excludes infants from the count, conversations should strictly center on the number of occupants in relation to the lease agreement.

4. Can Residents Request a Reasonable Accommodation?

Yes, federal fair housing law allows residents to request reasonable accommodations to occupancy limits, even if those limits are established by local ordinances. For example, if a resident requires live-in care due to a disability, the property manager may need to allow an additional occupant in the unit beyond the standard limit. When local regulations and federal civil rights laws conflict, federal law takes precedence.

Need a Lease Agreement?

A FREE account gets you access to over 200 free forms. Upgrade to a paid account (monthly, annually, or lifetime)

EZLandlord Forms Is Offering 15% 𝙊𝙛𝙛 For New Customers!

We cannot recommend these guys enough!

👉 State Specific Leases 👉 400 Forms to make your landlord-tenant relationship top notch 👉 200 FREE forms for those not ready to purchase 👉 4.8 Rating with over 5000 Reviews 👉 Pro Members get access to ALL leases and forms for $12 per month OR $75 if you purchase the annual membership 👉 YOU CAN BUY LIFETIME FORMS for $399

USE CODE 𝐒𝐓𝐀𝐂𝐈𝐄𝟏𝟓 to get 15% OFF ALL first-time purchases, EVEN THE LIFETIME FORMS!

Balancing Enforcement and Fair Housing Obligations

Enforcing occupancy limits is a necessary aspect of property management, but it must be done with an awareness of legal obligations under federal fair housing laws. By ensuring that occupancy limits are fairly applied and that reasonable accommodation requests are carefully considered, property managers can navigate this complex issue with confidence.

Reviewing occupancy policies regularly, staying updated on changes to housing laws, and providing ongoing training for staff are essential steps in maintaining compliance and fostering an inclusive and safe residential community.

In conclusion, property managers must find the right balance between enforcing occupancy limits for the benefit of all residents and accommodating individual needs under fair housing law. By maintaining open communication and staying informed of legal developments, property managers can ensure their policies are both effective and equitable.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

Stephen Michael White

Looking for marketing ideas to help you fill an apartment vacancy quickly? Maximize your rental property’s potential with our top marketing strategies. Discover how to fill vacancies fast, attract quality tenants, and enhance your apartment’s appeal in a competitive market. Turn your rental challenges into opportunities with our expert guide.

Key Takeaways

- Diverse Marketing Channels: Utilize a mix of advertising methods, including online listings, traditional signs, and word of mouth, to reach a broad audience.

- Engagement and Communication: Clearly articulate the benefits and features of your rental property to potential tenants, highlighting amenities and the local community.

- Strategic Pricing: Ensure your rental price is competitive within the local market to attract and retain tenants.

- Property Presentation: Keep the rental property well-maintained and attractive to prospective tenants, making a good first impression.

- Tenant Screening: Aim for quality over speed in tenant selection to ensure long-term stability and reduce turnover rates.

Finding the right tactics to market a new property is difficult, but filling vacancies is essential for any successful rental business.

A vacant rental property is like a pimple on the complexion of your real estate investment business—it’s all you can think about when it’s there, and you feel so much better when it’s gone!

Rental vacancies go even deeper. The longer you have vacancies you can’t fill, the more your bottom line suffers. Filling empty units is vital for long-term success, so finding the right strategies for your target market is essential.

Today, learn about five great ideas for marketing rental property that will fill your rental vacancies quickly.

Why Marketing Matters

For many new landlords, rental property marketing is something they have never had to do before. However, even more experienced landlords might still be searching for ways to successfully advertise an apartment for rent.

Before we learn the techniques that are helping landlords worldwide fill vacancies, consider why marketing should be a crucial element of your rental business.

Reduce Costs

When you have a vacant rental property, it costs you money every day that it sits empty, so it’s important to reduce that time between qualified, paying tenants to the bare minimum.

This is one of the most important reasons you should focus on rental property marketing in the early development stages of your business. Filling properties with good tenants can be challenging, but you want to ensure that you have a system to make this as efficient as possible.

Finding Good Tenants

While finding good tenants isn’t always the first thing on your mind when trying to fill a rental unit quickly, it is still an essential aspect of marketing. The more applicants you have for a property, the more likely you will find a good fit.

However, filling a vacant unit with good tenants takes more than printing neighborhood flyers.

How to Market Your Apartment for Rent: A Simple Guide

Once it is time to start marketing, there’s more to do than post your property in the right places. When learning how to market your apartment for rent, there are a few more things to know, including which method you use to market your vacant rental property.

Attend to The Rental Property

The rental property itself needs to be as attractive as possible. How much you can do and how early depends on whether an existing tenant currently occupies the unit or whether you are dealing with an already vacant unit. If the rental unit is currently occupied, coordinate with the tenant for a move-out inspection to get a good idea of what kinds of repairs and updates you’ll need.

It’s also an excellent time to photograph the rental property for your marketing efforts. Make a list of all the tasks you’ll need to do or manage to get the rental property in top shape.

Then, schedule services and maintenance the day after the tenant moves out so you don’t postpone a new tenant’s move-in date. Schedule the painters, carpet cleaners, and any other outside services as soon as you can so that the rental unit is move-in ready just a few days after being vacated.

With a rental property that is already vacant, you must still work quickly to get those outside services to transform the unit into something you can show prospective tenants as soon as possible. Remember that every day your rental property sits empty translates into zero income for you, so pressure everyone, including yourself, to get the property rent-ready.

Vacancy Tip:

Photographs of clean, empty rental units are generally more appealing to prospective tenants than photos of someone else’s furniture and belongings.

If you don’t have any photos of the empty rental property to use for your current marketing efforts, make sure you take the time during this transition to get some quality shots before the new tenants move in. You can keep these photographs on file to use the next time you need to fill a vacancy, saving yourself some time and hassle.

Write Enticing Marketing Copy

When advertising your rental property, your words and the features you highlight will motivate prospective tenants to contact you. Paired with good property photographs, the right marketing copy will tell applicants everything they want to know and help screen out people who wouldn’t be interested in your rental.

Make a list of all the features your rental property offers. Note the obvious things like the number of bedrooms and bathrooms and other details like the size, rent and deposit amounts, pet policy, location, and contact information.

List your property’s amenities and best features, such as laundry hookups, air conditioning, a pool, or new carpet. Then, think outside the box and decide what makes your property unique. In other words, what type of tenant would be attracted to it?

For example, mention that the property has easy freeway access or is close to downtown to attract younger professionals. You could list the elementary, junior high, and high schools for your single-family rental property to attract those with kids. Include anything you think might make your advertisement stand out from all the similar ones.

Vacancy Tip:

Nothing grabs attention better than the promise of a sale, discount, or other financial perks, so consider including that in your marketing copy headline. Examples include $100 off the first month’s rent, free six-month cable, or a $100 gift card upon signing a lease agreement.

Although it may seem counterintuitive to put up some of your own money or slash rent, it is a small price to pay to get the attention of prospective tenants and motivate them to choose your rental property over another.

Choose Your Advertising Avenues

Once ready to market your vacant rental unit and have the photos and copy, consider your best marketing sources to deliver the message to the correct recipients.

To get maximum exposure, post your advertisement in as many free places as possible and as many paid-for places as is reasonable and affordable.

Marketing a vacancy means making as many qualified applicants as possible aware that your property is ready and waiting for them. There are several options for both free and paid marketing campaigns. Free marketing means that it either takes no money or a minuscule amount to market your rental vacancy, while other marketing efforts may cost you to use their services.

Beyond those free sources, consider how much it costs to hold onto vacancies versus how much it would cost you to do paid advertising. This will allow you to see if your budget has reasonable space for paid advertising to bring new eyes to your rental properties.

Here are five great marketing ideas that will fill rental vacancies quickly:

- Word of mouth: Sometimes, other tenants can be your best free resource when finding potential tenants. Let your other tenants know that you have a vacancy available, and let them spread the word among family, friends, and co-workers. You can even throw in a finder’s fee for a good referral, such as a discount on rent or a gift card.

- Signs: Even if it seems cliché, putting up one or two “For Rent” signs can capture local traffic like nothing else. Put a sign in a prominent window or even on the front lawn to get the attention of pedestrians and motorists who frequent your neighborhood.

- Online listing sites: Many well-known websites with local market classifieds, including Craigslist and Zillow, are free. Look around for local or regional sites that include apartment and rental property listings, too. Social media platforms, especially Facebook Marketplace, is another good option.

- Online newspaper ads: Most newspapers have added an online version and still offer listings for a range of things, such as jobs, pets for sale, homes for sale, and rental vacancies. Check out your city or region’s local newspaper online and see what it would take to list your property. Most newspapers charge a nominal fee for a set timeframe. Usually, you can easily extend the listing if you have not found the right tenants.

- Local rental and real estate offices: It’s common for more prominent real estate offices to handle rentals and their advertising, but it will cost you a fee that varies from location to location. Real estate offices that facilitate rental referrals enjoy supplemental income. Additionally, it helps them make more contacts if your current tenants eventually become homebuyers.

Don’t Forget to Spruce Up Your Listing

When putting your listing online among many other rental property listings, it often feels like there’s no way to compete. After all, many properties are managed by experienced property managers with the latest camera gear and marketing language.

Still, you can help your listing be viewed positively by making a few minor changes. For example, various new technology is changing how people market their rentals.

We’re talking about 360-degree virtual tours of rentals and houses for sale.

Before You Start Marketing Your Vacant Apartment

Before you start marketing your company’s rental property, it’s essential to understand when to start and how to prepare. For example, jumping into advertising when a property is vacant isn’t always the right choice, as this could leave a bad impression or attract under-qualified tenants.

When to Start Marketing

It’s important to fill that empty unit as soon as possible, but not so fast that you miss essential and wise steps in recruiting and selecting prospective tenants.

If you currently have a tenant in the property, it won’t be easy to consider advertising until you are sure your tenant is moving out.

Ideally, your current tenant will give you a 30-day notice that they’ll be moving. This is the best-case scenario because you still have an occupied property for that month while you begin marketing to find a new tenant.

Sitting on a vacant unit for days, weeks, or months will only eat into your profits; when there’s no rent, your bills still need to be paid. Deliver a written notice to your current tenant to ensure they know you will show the rental property to prospective tenants over the next 30 days.

Remind the tenant of your state laws that allow you as the landlord to do this as long as you provide proper notice. Most states only require that landlords deliver a 24- or 48-hour written notice to the current tenant before showing the property.

If your tenant has abandoned the rental property or otherwise vacated without much notice, you’ll be aware of the ticking clock looming over your vacant property.

Consider Your Rental Pricing

Before starting your marketing efforts, take some time to ensure your rental unit is priced right. This means ensuring that the rent you charge for the unit aligns with your city or neighborhood and reflects a rate similar to those of your direct competitors—not too high or too low.

Rather than guess what rents are in your area, look at what your competition is asking, talk to local real estate experts, and even tour other properties if you can. The rent needs to be competitive for your area to attract tenants; otherwise, it could sit vacant while landlords all around you are filling up.

Speed vs. Quality: What Wins?

Filling a vacant rental quickly is every landlord’s dream, but don’t discount the long-term benefits of taking the time you need to get a quality tenant. If you ignore your standard tenant screening and interview process, you could lose more money in the long run on a bad tenant than you would by letting the property sit vacant for a bit longer.

Think of it this way: If you ignore your standard procedures for marketing, tenant screening, and interviewing and fill a vacancy quickly with someone you haven’t properly checked out, you increase your risk of filling the unit with a bad tenant. A bad tenant is more likely to either not pay rent or do something to get evicted.

The eviction process can take up to two months, during which time you will probably not collect rent. Take a few extra days or weeks to ensure you get the best tenant possible, who is the least likely to cost you.

Finding that balance between speed and quality is essential to ensure your real estate investment pays off.

Finding The Best Tenant

As mentioned, it’s about more than speed, as you still want a quality tenant in your rental.

We use QuickBooks daily in our rental property business!

It’s used to invoice tenants for their rent, track expenses by property and unit number, and our tax advisor can log on anytime to get information he needs for processing taxes or analyzing our data for goal setting meetings!

QuickBooks is the #1 accounting software for small businesses, and today you can take advantage of 30% off your first 6 months of QuickBooks Online using our exclusive Business Affiliate link.

Rental Property Marketing FAQs

How Can Landlords Effectively Market Their Rental Properties to Fill Vacancies Quickly?

Landlords can fill rental vacancies quickly by utilizing various marketing channels, such as online listings, word of mouth, and signage. Effective marketing also involves clear communication of the property’s benefits, competitive pricing, maintaining the property’s appeal, and careful tenant screening to ensure long-term occupancy and satisfaction.

What Do You Put On A “For Rent” Sign?

Once you start preparing some For Rent signs, you might suddenly realize you don’t know what to put on them! This is often a point of confusion for landlords. On the one hand, you will be tempted to put many details on the sign so that people know what to expect. But, on the other hand, you want the sign to be legible even at a distance.

How Can You Balance These Two Things?

The best thing you can do is keep the simple facts on the sign in large, bold letters visible at whatever distance the sign will most commonly be viewed. For example, you want signs that will be viewed from the road to have a larger font than a sign hanging on a door that people walk right up to.

The most important things to include are:

- The words “FOR RENT”

- Your phone number

That’s it! That’s all the information you must include, especially when the signs are viewed from a distance. Another benefit of keeping the information simple is making these signs professionally and reusing them for multiple rental properties.

Of course, making up some signs with more detailed information can also be beneficial. When making a sign that will be hung up close to its viewers, add the following in list form:

- Property address

- Rental price

- Application information

- Number of bedrooms and bathrooms

- Included amenities

- Other features

These long-form signs should include anything that will attract more applicants.

How Can I Make My Rental More Appealing?

Determining how to make your rental property more appealing to potential tenants is a good start when filling vacancies. However, a few approaches need to be considered when facing this situation.

First, consider whether actual changes and improvements must be made to your property. In some cases, properties will sit vacant because they do not meet the expectations of renters in the area. For example, a kitchen with outdated appliances might not rent well in an area where people want more modern, updated designs.

Take some time to review your property in comparison to what is actively renting in your area. Often, investing in these improvements will make your property easier to rent in the long term. Something as simple as painting the interior may be what it takes to find a renter.

Next, consider if you need to change how you advertise your property. Look over the following aspects of your rental property marketing to see if improvements can be made:

- Are your photos clear, showing a clean and welcoming rental unit?

- Does any writing copy include appealing features and local amenities that may attract buyers?

- Are you posting the advertisements in places where your target audience will see them?

- Have you recently updated the copy so that outdated information isn’t being used repeatedly for properties that have been vacant for some time?

Approach your rental marketing like a puzzle that you can solve. The key is determining what aspect of your rental is causing the vacancy. The way to find it is by troubleshooting with these techniques!

How Do You Attract Tenants In A Tough Market?

When competing in a high-volume rental or similarly competitive market, you might have difficulty filling vacancies as quickly as you would like. To attract tenants in a tough market, offer compelling amenities like dedicated parking and flexible lease terms. Though this is a complex problem to overcome, here are some additional tips that can be used to bring in more rental applicants:

- Add pet-friendly options to your apartment listing. This is becoming less common, so having this feature can be a real selling point.

- Upgrade appliances to be more energy efficient. Tenants will appreciate the potential cost savings and the earth-friendliness.

- Offer parking options, especially if you are in an area where parking is a real commodity. This might take some time, but it is worth the investment as it can attract many applicants.

Each proposal involves examining the area and considering what other rentals are lacking. What makes applicants jump on a listing quickly? If you can identify this it-factor in your area, you can set yourself up for fewer vacancies.

How Do You Attract High-Quality Tenants?

Finding tenants who fit your target audience can be difficult, and landlords of all experience levels need help. What is the right way to attract high-quality tenants?

First, you want to ensure you allow your rental applicants to show what type of tenant they would be. Rather than having an open house, try scheduling individual apartment tours. These tours will give you a chance to get to know the potential tenant, show the property thoroughly, and answer any questions they have.

High-quality tenants often know precisely what they want and aren’t afraid to ask questions. Engaging in one-on-one conversations can help you secure their application.

Additionally, ensure you require a full rental application, a background check, and an application fee. Not all landlords will agree that a rental application fee is necessary, but having the applicants pay for their background check is a great way to test how serious they are about the property. The best tenants will be ready and willing to make this commitment.

Finally, continually learn from your experiences as a landlord. Potential applicants who meet you, see your listing, or interact with other tenants in your building will be able to see what type of landlord you are. When you show that you are a professional and considerate landlord, prospective tenants will be more likely to apply.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

Listen On:

Most landlords spend years building a rental portfolio — and almost no time planning what happens to it when they’re gone. Whether you have no estate plan in place or think you have everything handled, this episode may reveal a gap you didn’t know existed.

In this episode of the Your Landlord Resource Podcast, Kevin and Stacie walk through the most common estate planning mistakes rental property owners make — many of which they discovered firsthand when creating their own living trust. From assuming a simple will is enough, to forgetting to fund the trust as your portfolio grows, to mismatched documents between spouses, this conversation covers the practical and emotional side of getting your estate plan right.

They also cover two estate planning tools that many landlords overlook entirely: Power of Attorney and the stepped-up basis tax rule — and they explain why having a Standard Operating Procedures manual is just as important as the legal documents themselves when it comes to protecting your rental business and the people you love.

WHAT YOU’LL LEARN IN THIS EPISODE

- Why a will alone is not enough to keep rental property out of probate — and what actually is

- What a pour-over will is and why your attorney may have already included one in your estate plan

- The trust-funding mistake that catches landlords off guard as their portfolio grows

- What happens when spouses have mismatched trust documents — and why it matters more than you think

- How property titling can override your trust and your will

- What a successor trustee is and what they are actually agreeing to take on

- Why a Power of Attorney is a separate and essential document for rental property owners

- Who your Power of Attorney Agent should be — and why a family member may not be the best choice

- The stepped-up basis tax rule: why gifting property during your lifetime may cost your heirs more than you realize

- Why your Standard Operating Procedures manual is part of your estate plan — and what to include

- The questions to ask your estate planning attorney whether you are starting from scratch or revisiting an existing plan

LINKS & REFERENCES MENTIONED IN THIS EPISODE

Episode 6 – Standard Operating Procedures for Landlords

Power of Attorney Article – Your Landlord Resource

Rental Property Management Software with Digital Lease and Tenant Records Management:

Connect with Us:

🌎 Visit our website

📧 Subscribe to our newsletter.

👆Click this LINK to select from our FREE Landlord Forms and Doc’s

🤳Text Us SMS text to 650-489-4447. We love questions and love letters, hate mail not so much!

📩Email us at: [email protected], [email protected]

✔️Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

📱 Follow us on Instagram, Facebook, & join our private Facebook group

🎧 Listen & Subscribe on Apple Podcasts, Spotify, or your favorite podcast app

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

Estimated reading time: 3 minutes

Listen On:

Most landlords don’t think twice when a teenager has been living in their rental for years. But the moment that kid turns 18, something quietly shifts — and if you’re not paying attention, it can cost you.

In this Shorty episode of the Your Landlord Resource Podcast, Kevin and I dig into one of those landlord blind spots that doesn’t announce itself until something goes wrong. We’re talking about what actually happens — legally and practically — when a minor living in your rental unit becomes an adult, and why doing nothing about it is one of the riskiest moves you can make as a self-managing landlord.

Here’s what surprises most people: screening an 18-year-old occupant has nothing to do with income. You’re not evaluating whether they can pay rent — their parent is still responsible for that. What you are doing is finding out if this adult, who now has zero legal obligation to you, has any background history you should know about before letting the situation continue unchecked.

We share two real stories from our own experience — including one from our own portfolio that, honestly, we’re still a little embarrassed about — and walk through the difference between adding a young adult as a full co-tenant versus using an adult occupant addendum, and why that distinction matters more than most landlords realize. We also talk through what happens when something catastrophic occurs with the primary leaseholder, and why having the right lease language in place before that birthday arrives can save everyone from an impossible situation.

If you have a tenant with a teenager living in your rental — or you’re drafting a new lease and kids are part of the household — this one is for you.

WHAT YOU’LL LEARN IN THIS EPISODE

• Why an 18-year-old living in your rental is legally an adult — and what that means for your lease

• The critical difference between an occupant and a leaseholder, and why it matters the moment that birthday hits

• Why you should screen adult occupants even when income doesn’t apply — and exactly what you’re screening for

• The adult occupant addendum: what it is, why it’s the better middle ground, and how EZ Landlord Forms and TurboTenant can help

• What happens if you add an 18-year-old as a full co-tenant — and when that’s the wrong move

• Two real-life stories: one from our own portfolio, one from advising a family member — and what we’d do differently

• The near-miss clause: why ‘added to the lease’ means nothing without the sentence that follows it

• What a succession clause is and why landlords should consider adding one

• Six specific things your lease should address before a minor in your unit turns 18

• Why verbal agreements don’t exist — and what to do instead

LINKS & REFERENCES MENTIONED IN THIS EPISODE

Episode 120 – When Roommates and Domestic Abuse Collide

EZ Landlord Forms – Amendment to Add Tenant / Adult Occupant Addendum

TurboTenant – Lease Addendum Tools

Connect with Us:

🌎 Visit our website

📧 Subscribe to our newsletter.

👆Click this LINK to select from our FREE Landlord Forms and Doc’s

🤳Text Us SMS text to 650-489-4447. We love questions and love letters, hate mail not so much!

📩Email us at: [email protected], [email protected]

✔️Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

📱 Follow us on Instagram, Facebook, & join our private Facebook group

🎧 Listen & Subscribe on Apple Podcasts, Spotify, or your favorite podcast app

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

Estimated reading time: 4 minutes

By John J. Stromberg

Whether you own one or multiple rental properties, a power of attorney is a key component in your estate planning portfolio.

Power of Attorney in General

A Power of Attorney takes effect on its execution date, remains in effect if you become incompetent and financially incapable, and expires when you pass away. Alternatively, a Power of Attorney document can set forth an earlier date upon which the authority granted therein will terminate.

Your Power of Attorney “Agent”

Your “Agent” is the person designated in your Power of Attorney to manage your estate if you become incompetent or financially incapable. An Agent can be someone close to you, such as a spouse, child, or parent. However, rental property owners may more prudently choose a business partner or another rental industry expert as the Agent. The designated Agent should ultimately acknowledge their duty by signing a certification and acceptance of authority.

Authority Granted in Power of Attorney

Agents have authority to handle matters ranging from business operations, claims and litigation, taxes, and real property transactions. For rental property owners, the Power of Attorney document can describe how your Agent should manage your assets to keep things running smoothly.

Estate Planning You Can Trust

Simple. Easy. Trusted.

Nolo’s WillMaker is America’s #1 estate planning software. Get immediate access to easy-to-use software and create your customized will today. Make a living trust, healthcare directive, power of attorney and so much more. There’s never been an easier, more affordable way to protect your family, home and assets.

Transferring Assets to a Trust through Power of Attorney

A Power of Attorney can simplify the transfer of assets into a trust by enabling your Agent to transfer those assets on your behalf. For example, if you’re unable to finish funding your trust due to an unforeseen severe accident, the Agent can make the necessary transfers for you. If a Power of Attorney is not in place before you become incompetent or pass away, the remaining assets not already in the trust may need to progress through the probate process.Click to Learn More About How to Protect Your Family and Assets

Power of Attorney Compensation

Your Agent is entitled to reimbursement for reasonable costs incurred in exercising their powers outlined in your Power of Attorney. Reimbursement of these costs may come from the assets your Agent is managing while you are incapacitated.

A Power of Attorney is a crucial component in any rental property owner’s estate planning toolbox.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

by Ryan Squires

Profit and loss statements (P&L) are one of the key reports rental property owners need to run their businesses. Also known as the “rental income statement” or “income expense statement,” this report summarizes a business’s transactions and calculates the profit (or loss). It shows where money is coming from and going to over a specified period.

Analyzing profit and loss is essential for landlords and property managers, so understanding the basics of the report is crucial. Today, we’ll discuss what you’ll find in an income statement, how to calculate profit or loss for your property, how to use P&Ls within your business, common mistakes to avoid, and more.

What’s included in a profit and loss?

P&L reports cover a set period and include the income, expenditures, and net operating income calculation for that time. The statement consists of three parts: gross income, operating costs, and net operating income. Do you have more than one property or unit? If so, you’ll need a P&L with a column for each door.

Section 1: Gross Rental Income

Gross income is the total revenue generated by the rental property before you deduct any expenses. So in this section, you’d include the unit’s rents plus any additional income associated with the property:

- Application fees

- Late charges

- Laundry fees

- Lease renewal fees

- Parking charges

- Pet fees

- Rents

- Storage charges

- Vending machine income

If you offer additional services, like meal options, concierge services, or transportation, that aren’t typically included in the rent, that income is included in a P&L statement, as well.

Key point: Record security deposits on your balance sheet, not the profit and loss statement. Security deposits only count as income if your tenant breaches the lease terms and you retain some or all of the security deposit. A refundable deposit that you’re holding until the lease ends isn’t reportable income.

Section 2: Operating Expenses

This section reports the costs associated with the day-to-day operations of your rental property. Your P&L report uses the chart of accounts categories to group expenditures, so the expense section of a rental property P&L frequently aligns with the IRS Schedule E categories:

- Advertising

- Auto and travel

- Cleaning and maintenance, including landscaping, snow removal, and pest control

- Commissions

- Insurance

- Legal and professional fees, including accounting costs

- Management fees

- Mortgage interest

- Repairs

- Supplies and small equipment

- Taxes, like property or sales tax, not income taxes

- Utilities, including phone, internet, and garbage collection

- Other, such as education, dues, subscriptions, licenses, etc.

Capital improvements, fixed assets, and loan principal repayments won’t show in this section; those belong on your balance sheet instead.

Section 3: Net Operating Income

Net operating income (NOI) shows the profitability of your investment property. The formula is simple:

Income − Expenses = NOI

Note: NOI is your before-tax income; in other industries, this figure is also known as EBIT, which stands for earnings before interest and taxes.

Despite its straightforward formula, NOI—and the income statement—play a key role in running your rental property business.

How to Use a P&L for Rental Property

With the information from your income statement, you can answer questions and gain insight into your property’s performance. Why is the rental over- or underperforming? Which areas of the business should you target to reduce costs? Which income streams are most profitable? Use your P&L for more than just assessing profitability—here’s how.

Evaluate Your Property’s Financial Health

For real estate investors, understanding a property’s financial health is essential, and your P&L statements are a key part of that. You can use the NOI to evaluate your investment, compare properties, and gauge their performance. The higher your NOI, the more profitable the property.

You can also analyze your P&L to look for income and expense trends. Creeping costs and dwindling income affect your profitability over time, so reviewing your statements regularly will help you catch issues early on.

Perform Comparative Analyses

Are you looking to expand your portfolio? Use the P&L statements from the properties you’re considering for a comparative analysis. The income statements will help you identify the property with the best return or most consistent revenue streams.

By reviewing the P&L statements for potential investments, you can also evaluate the potential risk for each property by asking questions. Is the income stable? Do the expenses fluctuate significantly? What are the market trends?

Appraise Properties and Secure Financing

Once you know a property’s NOI, you can appraise the rental unit by calculating its cap rate, which measures a property’s rate of return and helps you estimate a property’s fair value.

Having a healthy P&L also makes it easier to secure funding and more favorable financing terms. NOI can affect loan approval because lenders use it to assess your cash flow as part of the debt service coverage ratio.

This metric gauges your ability to repay debts, including repaying principal and interest on long- and short-term debt. Investors also use this ratio and a property’s NOI to make informed decisions about acquisitions, sales, or refinancing.

Manage Risk and Make Strategic Plans

Analyzing your P&L is another way to detect and mitigate financial risks for your rental property business. When you review your income statements regularly, you’re searching for potential issues.

For instance, if your utility costs are up unexpectedly, that might indicate a leak that your renters haven’t noticed or reported yet. By addressing the leak early on, you prevent a bigger, more expensive problem later on, thereby reducing your risk.

You can project the income and expenses for your investment property by reviewing the P&L and net operating income. These projections help you update your budgets, prepare for taxes, and form long-term investment plans, such as future improvements, refinancing, or property acquisitions. Based on market shifts and property performance trends in your P&L, you can adapt your strategies.

How to Calculate Profit or Loss on Rental Property

The net operating income formula is simple:

Revenue – Expenses = Profit (or Loss)

The difficulty lies in setting up the report, then tracking and recording the transactions that affect the income statement.

How to Set Up an Income Statement for Rental Property

The categories in your chart of accounts are used in the P&L, so the more detailed your chart of accounts, the more detailed your P&L may be. Just remember that too many details can complicate your reports or cause confusion. You don’t need an income line for each tenant from one property or an expense line for each vendor.

Think about what would be most helpful for your business, then refine your chart of accounts and reports to support your needs.

Pro tip: Aligning your chart of accounts and P&L with the Schedule E makes tax prep simpler.

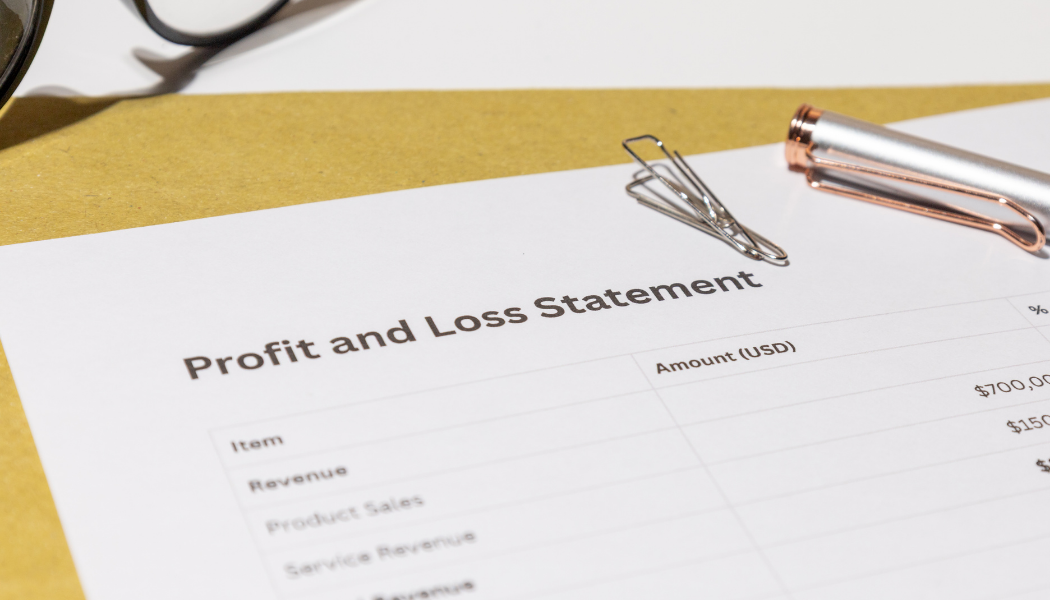

Sample Income Statement for Rental Property

| Account | July 2025 |

|---|---|

| Income | |

| Rental Income | $1,500 |

| Late Fees | $0 |

| Pet Fees | $100 |

| Parking Fees | $50 |

| Total for Income | $1,650 |

| Expenses | |

| Advertising | $100 |

| Auto and Travel | $80 |

| Cleaning and Maintenance | $275 |

| Commissions | $0 |

| Insurance | $100 |

| Legal and Professional | $0 |

| Management Frees | $0 |

| Mortgage Interest | $75 |

| Repairs | $50 |

| Supplies | $20 |

| Taxes | $0 |

| Utilities | $200 |

| Other | $50 |

| Total for Expenses | $950 |

| Net Operating Income | $700 |

Beginner landlords often use templates or spreadsheets to create income statements, and many (but not all) property management or accounting platforms include the profit and loss statement in their reporting options.

A landlords one stop shop for tenant management…for FREE

You can’t beat free and the only time you pay is if you want to purchase a lease or have expedited rent deposits. Most everything else costs zip, zero, zilch.

Why do landlords need different versions of the P&L?

By reviewing different versions of your rental’s income statements, you’ll gain different perspectives of the property’s performance. These are the four most commonly used versions of the income statement for real estate investors.

Monthly

This version shows your property’s data for a single month. This snapshot view makes it easier to spot unexpected costs and irregularities.

Year to Date

The year-to-date income statement shows total income, current expenses, and NOI for the year so far. This version helps analyze overall performance and is a good indicator of your current taxable income.

Pro tip: A year-to-date P&L broken down by month makes it easier to spot trends in income or costs and budget variances.

Year-End

The annual, or year-end, income statement shows the property’s total income, costs, and NOI for the tax year. Use this version to prepare annual budgets and taxes, as well as to update key performance indicators, such as the cap rate.

Trailing 12 Months

Also known as the TTM or T-12, this form of the income statement covers the property’s performance over the last year from the current date. Use the T-12 to monitor the change in your property’s NOI.

Need a loan or mortgage? The lender may want to see a T-12, T-3, and rent roll.

Common Mistakes with Rental Property P&Ls

You want your rental property to be as profitable as possible, and your P&L can help you make that happen, as long as you avoid these common errors:

Not Classifying Transactions

Reports are only helpful if they’re accurate. Uncategorized income or expenses make it difficult to prepare reports, file taxes, and make informed decisions about the property.

Using P&L Spreadsheets and Templates

Spreadsheets require time to update and attention to detail for manual data entry. Problems with formulas or math errors can lead to missed deductions and incorrect reporting. Plus, each property needs a column on the P&L—every version. That’s a significant time commitment with considerable potential for errors.

Not Recording All Income

Sometimes landlords aren’t sure what counts as reportable rental income, so they don’t record some transactions. But if you leave transactions off your books, you don’t have complete records or full transparency in your business. And over- or underreporting income can have serious consequences, including IRS penalties and interest.

Skipping Report Reviews

Tempted to skip reviewing your reports? This mistake is easy to make if you’re short on time. But if you don’t review your reports regularly, you can’t make informed decisions. You’ll lose the chance to monitor your cash flow, key performance metrics, and income and expense trends. And you won’t be able to identify and correct potential issues or adjust your budgets and long-term plans.

Deducting Fixed Assets in Full

Fixed assets, or capital improvements, are significant investments that add value or extend the property’s useful life. These improvements are not fully deductible in the year they’re incurred, except under particular circumstances. So when you invest in a fixed asset, like a new roof or furnace, the purchase shows on your balance sheet, not the profit and loss.

You can recoup the cost of the asset through depreciation, a noncash expense that will show on your P&L. Incorrectly deducting fixed asset purchases will have a significant effect on your books—greatly reduced profitability—and it opens you up to IRS penalties if you get audited.

How TurboTenant Can Help

The income statement is a critical element for managing your rental property, so why rely on time-consuming, error-prone templates?

Skip the spreadsheets and save time with TurboTenant, rental property management software with an integrated accounting platform. We’re here to simplify bookkeeping and property management for your rentals.

Our platform is better than using outdated spreadsheets—no more manual data entry or fighting with formulas! Linked accounts, automatic imports, and customizable rules allow you to automate your account updates while ensuring accuracy.

Not an accounting whiz? No problem.

Unlike expensive generic accounting platforms, our bookkeeping software is designed especially for rental property investors like you. You don’t need an accounting degree or a bookkeeping background to use TurboTenant’s accounting and bookkeeping features.

Your chart of accounts is preconfigured for real estate, right from the first click. Plus, we’ve got transaction templates ready to help you correctly record items like security deposits or mortgage payments.

Stay on top of your rental’s financials with built-in reports, including balance sheets, rent rolls, cash-on-cash, and multiple P&L statements, all available at the unit, property, and portfolio level. We’ll help you get ready for tax time, too, with deduction reviews, Schedule E reports, and accountant access.

Say goodbye to spreadsheets and generic accounting options, and save yourself time, money, and headaches.

Sign up for a free TurboTenant account today!

Disclaimer: This blog is for informational purposes only and is published by TurboTenant. It is not legal, financial, or tax advice. Laws and regulations for landlords vary by state and locality and may change over time. Always consult a qualified attorney, accountant, or local housing authority before making decisions related to your rental property. The publisher and authors assume no responsibility for actions taken based on the information provided.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

Listen On:

Most landlords know they need photos to market a vacant rental. But if that’s the only time your camera comes out, you’re leaving serious money — and legal protection — on the table.

In this episode of the Your Landlord Resource Podcast, Kevin and I dig into why rental property photos are one of the most underutilized tools in a self-managing landlord’s toolkit. From attracting quality tenants to winning security deposit disputes, the right photos taken at the right time can make all the difference in how you operate your rental business.

We share a real story from our own portfolio — a move-out that was anything but clean — and how our documentation photos saved us from a potential dispute. We also get into the debate between smartphone photography and hiring a professional, and Kevin walks through exactly how he takes our listing photos to get the best results without spending a dime on a photographer.

Whether you’re a new landlord building your systems or a seasoned property owner who’s been winging it on photos, this episode will give you a clear, practical framework you can put to work immediately.

WHAT YOU’LL LEARN IN THIS EPISODE

- Why rental property photos are about much more than filling vacancies

- How great listing photos attract better tenants and help justify your rental price

- Why poor or missing photos can signal weakness to manipulative applicants

- How to use photos as legal protection for security deposit disputes and lease violations

- The four (and sometimes five) critical times you should always have your camera out

- When a smartphone is enough — and when to hire a professional photographer

- Kevin’s exact method for taking consistent, high-quality listing photos

- Why still photos are preferred over video in small claims courts

- How to organize your photo storage so you can find evidence fast when you need it

- The smart way to use property videos — and why they’re great for pre-qualifying showings

LINKS & REFERENCES MENTIONED IN THIS EPISODE

Episode 23 Tips on Marketing Your Rental Property

Blog Post: Tips for Taking Great Rental Property Photos

Kevin’s Tripod Used for Marketing Photos

Kevin’s Gimbal (for video walkthroughs)

Connect with Us:

🌎 Visit our website

📧 Subscribe to our newsletter.

👆Click this LINK to select from our FREE Landlord Forms and Doc’s

🤳Text Us SMS text to 650-489-4447. We love questions and love letters, hate mail not so much!

📩Email us at: [email protected], [email protected]

✔️Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

📱 Follow us on Instagram, Facebook, & join our private Facebook group

🎧 Listen & Subscribe on Apple Podcasts, Spotify, or your favorite podcast app

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

Estimated reading time: 3 minutes

Listen On:

Running rental properties efficiently often comes down to having the right systems in place. In this episode of the Your Landlord Resource Podcast, Kevin and I walk through one of the most effective landlord systems we’ve created for our rentals — our unit binder.

A unit binder for landlords is a simple system we place inside every rental unit that answers common tenant questions, explains how appliances work, and provides helpful information about the property. Over time, this landlord system has dramatically reduced tenant questions, prevented unnecessary maintenance calls, and helped our tenants handle everyday situations more independently.

Inside the binder we include property information like trash schedules, parking rules, inspection expectations, and appliance care instructions. We also use QR codes that link to short instructional videos so tenants can troubleshoot common issues without needing to contact us.

What started as a simple idea has turned into one of the most valuable landlord systems we use in our rental business. It helps our tenants feel supported while also allowing us to manage our properties more efficiently.

If you’re a self-managing landlord looking to reduce tenant questions, prevent maintenance issues, and operate your rentals more professionally, this episode will walk you through how our unit binder system works and how you can build one for your own properties.

WHAT YOU’LL LEARN IN THIS EPISODE

• What a unit binder for landlords is and how it works

• Why landlord systems help reduce tenant questions

• What information to include in a rental unit binder

• How appliance instructions can prevent maintenance issues

• Why QR codes and instructional videos improve tenant independence

• How property information like parking and trash schedules helps tenants

• Why proactive systems improve rental property management

• How landlord systems save time and prevent costly repairs

If you enjoyed this episode on Landlord Systems: The Unit Binder, you may also find these episodes helpful:

Essential Communication Methods Every Landlord Should Know – Episode 87

Strong communication systems help landlords stay organized and respond consistently to tenant questions.

https://YourLandlordResource.com/episode87

Roommates as Tenants – Episode 119

Learn how clear expectations, agreements, and documentation can prevent disputes between tenants sharing a rental.

https://YourLandlordResource.com/episode119

Why Rental Property Inspections Matter – Episode 4

Routine inspections are another important landlord system that helps prevent maintenance issues and protect your property.

https://YourLandlordResource.com/episode4

LINKS & REFERENCES

Episode 119 Roommate Tenants and Why We Don’t Prefer Them

KwikSet Halo Smart Lock Touchscreen & Deadbolt:

Kwikset Halifax Passage Doorknob

Emergency Gas Shutoff Wrench

Connect with Us:

🌎 Visit our website

📧 Subscribe to our newsletter.

👆Click this LINK to select from our FREE Landlord Forms and Doc’s

🤳Text Us SMS text to 650-489-4447. We love questions and love letters, hate mail not so much!

📩Email us at: [email protected], [email protected]

✔️Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

📱 Follow us on Instagram, Facebook, & join our private Facebook group

🎧 Listen & Subscribe on Apple Podcasts, Spotify, or your favorite podcast app

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

Estimated reading time: 0 minutes

Listen On:

Owning rental property isn’t just about collecting rent — it’s about running a service-based business. And whether landlords realize it or not, their tenants are customers. The way you communicate, handle maintenance, and manage the living experience inside your rental property can directly impact tenant satisfaction, lease renewals, and the long-term success of your rental business.

In this episode of the Your Landlord Resource Podcast, Kevin and I talk about why customer service is such an important part of being a landlord. Many owners assume the best strategy is to simply stay out of the tenant’s way and only respond when something goes wrong. But in our experience, landlords who focus on communication, responsiveness, and professionalism tend to build stronger tenant relationships and experience fewer problems over time.

We share real examples from our own rental properties about responding to maintenance requests, communicating repair plans, notifying tenants about work being done on the property, and creating clear communication procedures. We also discuss why tenants should always have a backup contact when landlords are unavailable and how small gestures — like welcome gifts or birthday cards — can make tenants feel valued.

These simple practices may seem small, but they can make a significant difference in how tenants perceive their landlord and their living experience.

If you want to improve tenant relationships, reduce turnover, and run your rental property more professionally, this episode will give you practical ideas to strengthen the customer service side of your rental business.

WHAT YOU’LL LEARN IN THIS EPISODE

• Why rental property ownership is a service-based business

• How customer service affects tenant satisfaction and lease renewals

• Why responding quickly to maintenance requests matters

• How communicating repair plans protects both tenants and landlords

• Why notifying tenants before property work builds trust

• Why landlords should provide alternate contact information when unavailable

• How tenant referrals can help attract better applicants

• Why small gestures like welcome gifts can strengthen tenant relationships

• Communication strategies that help landlords stay professional and consistent

• How good customer service can reduce tenant turnover

LINKS & REFERENCES

Episode 87 Essential Communication Methods Every Landlord Should Know

3M Claw Picture Hanger

Connect with Us:

🌎 Visit our website

📧 Subscribe to our newsletter.

👆Click this LINK to select from our FREE Landlord Forms and Doc’s

🤳Text Us SMS text to 650-489-4447. We love questions and love letters, hate mail not so much!

📩Email us at: [email protected], [email protected]

✔️Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

📱 Follow us on Instagram, Facebook, & join our private Facebook group

🎧 Listen & Subscribe on Apple Podcasts, Spotify, or your favorite podcast app

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

Estimated reading time: 3 minutes