By Deirdre Mundorf

Know your rights as a tenant—and limitations as a landlord. While landlords hold a lot of power, there are several things they are not legally allowed to do.

Whether you are looking to rent an apartment or considering buying a rental property, it is essential to know what landlords are and are not allowed to do. Just as landlord rights protect landlords, tenants also have rights. Understanding what a landlord cannot do will protect you from being treated unfairly as a tenant and prevent you from crossing a legal line when renting a property. Read on to learn more about some of the laws that landlords must follow when renting their property. Keep in mind that landlord tenant law provisions can vary by state, so before renting to or from someone, read up on the local landlord and tenant laws in your state.

1. Use Discriminatory Practices

{kind=link}

Photo: istockphoto.com

While landlords may choose to use a tenant screening service, they may not use discrimination as the basis of any decisions regarding current or potential tenants. The Fair Housing Act states that any form of discrimination based on race, disability, color, religion, national origin, gender, sexual orientation, or familial status is illegal. If you feel like your landlord or potential landlord is using discriminatory practices, file a complaint on the HUD website or contact a local advocate in your state.

2. Enter the Property Without Giving Sufficient Notice

{kind=link}

Photo: istockphoto.com

A landlord may own the property, but that does not mean that they are able to enter it any time they wish. Most states have laws in place requiring landlords to provide their tenants with a minimum of 24 hours notice before they enter the property. In some states, they are required to provide written—not even via text or email—notice unless the tenant has agreed to the latter form of communication. Furthermore, landlords may only be allowed to enter a property (after providing sufficient notice) during regular business hours—9 a.m. to 5 p.m., Monday through Friday. Exceptions to this rule include emergencies or if the landlord suspects that the tenant has moved out and left the rental abandoned.

If your landlord has not been providing sufficient notice before entering your rental unit, start by making sure they are aware of the law. If this does not change their behavior, you can report them to the local housing office or even contact the police to file trespassing charges.

3. Evict Tenants Without Following Legal Guidelines

{kind=link}

Photo: istockphoto.com

Landlords have the right to evict tenants. However, there are limits to that right and a landlord is required to follow the proper procedures mandated by their state. In some states, they are required to give 30 days notice (or even more in some places), while other states do not require much, if any, notice to be given to the tenants before eviction can occur. If a landlord evicts a tenant without following their state’s procedures, it is possible that they could face burglary or trespassing charges. Contact your local housing authority immediately if you think your landlord evicted you without following the proper channels.

4. Raise the Rent in the Middle of the Lease Without Justifiable Cause

{kind=link}

Photo: istockphoto.com

Even though most landlords are renting property for income, they are not allowed to simply raise the rent in the middle of the lease to make more money. When you and your landlord signed the lease, you both agreed to the stated rent payments. Unless they have just cause—such as a roommate moving into the property or a new pet joining the household—they cannot simply decide to raise the rent before the lease is up.

5. Deny Requests for Repairs Related to Health or Safety

{kind=link}

Photo: istockphoto.com

While a landlord is not obligated to complete all requested repairs, they are also not allowed to refuse to complete repairs that are necessary for the health or safety of their tenants. If the property has mold, broken utilities, or other serious issues, the landlord will have to address them promptly. If you do not feel like your landlord is taking a concerning issue seriously, seek guidance from your local housing office.

Your Landlord Resource has teamed up with Toggle, a division of Farmers Insurance that offers competitive pricing of renters insurance for tenants.

Policies can start as low as $5 a month!

Copy and share our link with your tenants to get them started: http://go.gettoggle.com/SH1E Download this PDF to present to your tenants with your renters insurance request! Toggle Renters Insurance Flier.pdf

6. Rent a Room Without a Window

{kind=link}

Photo: istockphoto.com

If you’re considering living with private owners renting a room out, know that one of the rules for renting is that bedrooms must have a window or exterior door. In fact, it is illegal for anyone to rent a room that does not have a window. In order to qualify as a “bedroom” suitable for sleeping, a room must have an egress window or door that will allow the occupant to safely escape in the event of a fire. Homeowners are not allowed to rent out certain parts of their property, and this most certainly includes windowless rooms.

7. Charge Unreasonable Late Fees

{kind=link}

Photo: istockphoto.com

Late rent payments happen, and landlords are allowed to charge late fees. However, while landlord leasing requirements can vary by state, many include limitations on the fees that can be charged for late rental payments and may also specify a grace period for late payments. For example, states such as Maryland, New York, Delaware, Nevada, North Carolina, and Oregon only allow late fees up to 5 percent of the monthly rent. However, several states have no stated limit on the maximum late fee. If you live in one of these states—including Connecticut, Florida, California, Indiana, Colorado, and Louisiana—read your lease closely and do your best to make sure that you are on time with your rent payments to avoid being charged extra.

8. Withhold the Security Deposit Unjustly

{kind=link}

Photo: istockphoto.com

It is unlikely that you’ll find any landlords who do not require a security deposit. The security deposit is designed to protect landlords for both private owner house rentals and larger apartment complexes against damage that tenants cause to the property. Once the tenants move out, landlords can withhold some or all of the security deposit to cover necessary repairs, such as fixing something that was broken by the tenant. What they cannot do is withhold the security deposit to cover normal wear and tear, such as slightly worn carpet or a few scuff marks on the walls or floors.

9. Charge Pet Fees or Deny Housing for Individuals with Service Animals

{kind=link}

Photo: istockphoto.com

Landlords are not required to allow pets in their properties. And, if they decide that they are going to allow individuals with a cat or dog to live in their house, they have the right to charge a pet fee or an additional monthly rent payment. The exception to this, however, is for individuals who have a service animal. According to the U.S. Department of Housing and Urban Development, in nearly all cases, landlords cannot deny housing or refuse to accommodate an individual’s need for a service animal.

10. Raise the Rent in Retaliation of Something the Tenant Did

{kind=link}

Photo: istockphoto.com

If a landlord raises your rent after you made a complaint against them, they are likely breaking state law and the landlord tenant act. These laws are designed to protect tenants against retaliation after taking a legal action against their landlord, such as complaining about unsafe living conditions, following state laws to withhold some or all of the rent for uninhabitable conditions, or coordinating with other tenants to voice your views. Take action if you believe your landlord is raising your rent out of retaliation for something you did. Consider filing a suit in your local small claims court or making a complaint against your landlord to your local housing department.

FAQ About What a Landlord Cannot Do

Learn more about some of the limitations to the power a landlord holds by reading through the frequently asked questions below.

Q. Can a landlord raise rent during a pandemic?

Unless the city or state has put a rent freeze into effect because of the pandemic, landlords are allowed to raise rent.

Q. Can a landlord come on the property without notice?

No, in most states, landlords are required to give sufficient notice (typically 24 hours) before entering a tenant’s property.

Q. Do I need to have landlord insurance if I rent properties?

Landlord insurance is not required when renting a property. However, you may decide that the additional coverage provided by landlord insurance is worth the additional cost.

Q. Can a landlord kick me out?

Landlords have the right to evict tenants who do not follow the agreements set in the lease. However, in most states, they are required to give proper notice before executing an eviction.

Q. Do landlords forbid tenants to bring in animals?

Yes, with the exception of service animals, a landlord has the right to forbid their tenants from having animals in their rental unit.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

2023 was a volatile year for the multifamily industry.

Demand patterns and rent prices returned to a post-pandemic normal, but apartment communities’ operating expenses skyrocketed while nationwide occupancy rates declined.

Additionally, the supply of new units entering the marketplace drove up competition and gave renters more control in choosing where to rent.

Those issues are setting the stage as the industry turns the calendar. How will they impact your communities’ plans to attract, attain and retain residents? Let’s look deeper at the challenges owners and operators face in 2024 and how to overcome them.

Challenge #1: 2024 will be another record-breaking year of new unit deliveries.

According to Yardi Matrix, an additional 500,000+ new units will enter the marketplace in 2024, giving renters the upper hand by having more apartment choices than ever and undeniably impacting your existing communities’ ability to attract new residents.

Solution: Ensure your apartment’s digital marketing presence remains competitive by letting renters see the inside of your units.

The opening of a new apartment community nearby is less threatening when your apartments’ digital marketing presence prioritizes the needs of prospective renters. You’ll stand out in 2024 (and beyond) and make it easier for renters to choose your community when you make it possible for every renter to see the inside of the specific floorplan or unit they’re interested in on your apartment’s website and other online channels.

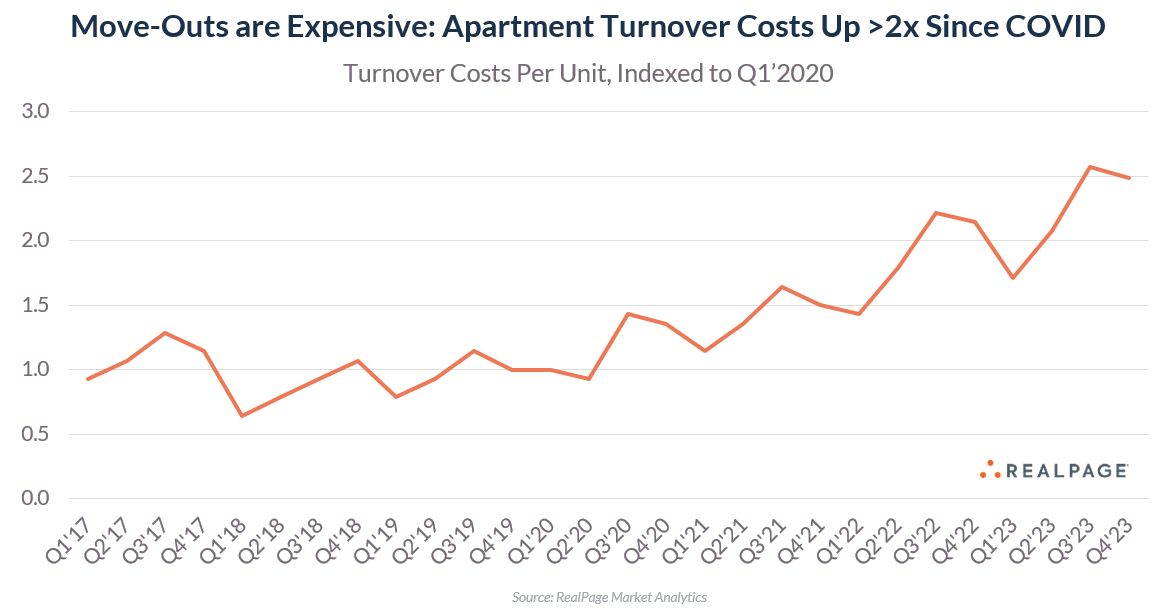

Challenge #2: Turnover costs are on the rise in 2024.

According to Jay Parsons, rental housing economist at RealPage, turnover costs have more than doubled since the COVID pandemic hit and can “easily exceed one month’s rent” of that unit. Alarmingly, the rising costs do not factor in marketing expenses or vacancy loss.

Solution: Make resident retention a priority by focusing on your renewal strategy.

Your lease renewal strategies in 2024 will be critical as you combat rising operational expenses. Treat renewal pricing as crucially as you would for a new lease and include any concessions, if necessary, such as offering renewal rates below what the current resident is paying.

Additionally, you must provide an excellent resident experience, as that, above anything else, is the best method for ensuring more residents choose to stay.

Looking for the next level of landlord software before handing off to a property manager?

Hemlane is a software that is built to grow with your needs as a landlord.

For a minimal amount, there’s a really good basic package but what we love is the option to upgrade and add 24/7 maintenance management on.

Hemlane offers complete financial support as well. You can link multiple bank accounts for direct deposit rent payments, add automatic late fees, sends reminder notifications to your tenants, and has a detailed profit and loss statement that can includes automatic and manual uploads of income and expenses.

It gets better! If you reach a place where you are ready to hand off management to a property manager, Hemlane has that too under their “Complete” option.

You can try Hemlane out FREE for 14 days (no credit card required) to see if it’s a good fit for you!

Challenge #3: Apartment marketers must generate leads with smaller budgets in 2024.

Many are responding to the increasing expenses of owning and operating a multifamily property by tightening their budgets, which sometimes include marketing and advertising. The fear is that reducing marketing investment could also reduce lead counts.

Solution: Develop the right mix of marketing channels for producing better-qualified leads.

Even though it may feel that you need more marketing tools and higher budgets these days to manage multiple channels, the truth remains that there’s a very typical pattern by which renters discover, engage, and eventually select an apartment. We call it the “Leasing Funnel,” or the mix of apartment marketing channels you can apply that puts your community front and center throughout a prospect’s search.

Following the Leasing Funnel as you establish your multifamily marketing plan for 2024 will make your marketing expenses more efficient and help prospects discover and learn essential information about your community online and feel more comfortable with making the life-impacting choice of where to rent an apartment.

Takeaways

- New Unit Boom: 2024 will see a record influx of new apartments, increasing competition and requiring stronger digital marketing with floorplan-specific visual content showcasing the inside of your units to stand out.

- Rising Turnover Costs: Combat skyrocketing turnover costs by prioritizing resident retention through competitive renewal rates and an excellent resident experience.

- Smaller Marketing Budgets: Optimize marketing efforts with the “Leasing Funnel” strategy, focusing on the right mix of channels to attract better-qualified leads while maximizing efficiency and return on investment.

Source: RentVision

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

By Krista Reuther

Are you new to the world of renting? Are you a landlord looking to diversify your portfolio? Or are you just curious about mid-term rentals?

No matter why you’re here, we’re glad you found us! We’ve put together this guide as an overview of everything you need to know about medium-term rentals.

In this blog, we’ll cover everything from what a mid-term rental is, how to go about their lease agreements, and who uses them. We’ll also talk about the pros and cons of managing mid-term rentals. Let’s dive in!

Table of Contents

- What Is a Mid-Term Rental?

- Who Uses Mid-Term Rentals?

- What You Need in a Mid-Term Lease Agreement

- What Are the Pros of Managing a Mid-Term Rental?

- What Are the Cons of Managing a Mid-term Rental?

- Conclusion

What Is a Mid-Term Rental?

You’ve probably heard of short-term and long-term rentals, but what exactly is a mid-term (or medium-term) rental? The answer is in the name: a mid-term lease agreement is a rental agreement between a property owner and tenant that lasts for less than one year but usually more than one month.

Ordinarily, short-term rentals last for less than one month (and are sometimes referred to as vacation rentals), while long-term rentals are typically year-long leases. Medium-term rentals fall into that sweet spot of at least one month but average three to nine months.

Mid-term rentals are ideal for landlords in highly populated cities or college towns. In addition to populous metropolises, medium-term rentals work well in areas where seasonal work is common, such as near agricultural centers. They’re also great for prospective landlords who want to get into the rental market but aren’t ready to have a long-term commitment.

Who Uses Mid-Term Rentals?

If you’re pursuing real estate investing, it makes sense that you’d want to maximize your return on investment. Mid-term rentals can offer a surprising return on investment despite frequent turnover. Mid-term rental demand is growing, especially with the post-pandemic rise in remote work creating the profile of a “digital nomad”. And of course, prolonged business trips and vacations will always create demand for flexible lease durations.

Let’s take a look at some of the most common groups of people that use mid-term rentals:

- Traveling nurses: At the height of the pandemic, traveling nurses needed housing like never before, and they’re still in high demand across the country. Rather than shell out exorbitant fees to live in a trendy Airbnb, mid-term rentals allowed nurses to establish a home away from home.

- Students: Students often need somewhere to stay while they attend class. Mid-term rentals provide students with an affordable option that doesn’t require them to live on campus or commute long distances daily.

- Digital nomads: Digital nomads are people who work from home or remotely and travel frequently as a lifestyle choice. They tend to be more transient than other travelers —they may stay with friends or family before finding a new location where they can settle down for a while.

- Business professionals: Many industries require their employees to travel. Some companies host workers in mid-term corporate housing; others seek their own mid-term housing solutions.

Other tenants who may use medium-term rentals include families relocating to a new city and professionals heading to a new place to start an internship. While all these groups may have different reasons for moving, they generally use mid-term rentals because they have reasonably extended short-term housing needs.

A landlords one stop shop for tenant management…for FREE

You can’t beat free and the only time you pay is if you want to purchase a lease or have expedited rent deposits. Most everything else costs zip, zero, zilch.

What You Need in a Mid-Term Lease Agreement

Mid-term rentals are unique in many ways, which means you’ll need to make sure your lease agreement reflects your specific rental. There are several things to consider when drafting a mid-term lease agreement, including but not limited to:

- The length of stay/occupancy (rental period of one to 12 months)

- The amount of rent

- Security deposit and other applicable fees

- Amenities – utilities like Wi-Fi access and whether the rental house is furnished or not

- Local landlord-tenant laws and regulations

- Tenants’ rights

- The responsibilities of both the tenant and landlord

Generally, medium-term lease agreements may not involve a lot of legal stipulations like traditional leases. However, check your local landlord-tenant laws to make sure you’re abiding by any specific term-based lease requirements. We also recommend that you chat with your attorney or local housing authority before any documents are signed to ensure you’re doing everything by the book.

What Are the Pros of Managing a Mid-Term Rental?

While long-term rentals can be great for owners looking for a steady rental income stream over several years, mid-term rentals offer unique advantages, including:

- You have access to new tenants who may be more willing to work with you and are less likely to default on their lease agreement than long-term tenants who have lived there for several years.

- Unlike short-term housing, you’ll have a more steady cash flow that is less susceptible to seasonal fluctuations.

- You have more flexibility since you don’t have to worry about a long-term commitment.

- Your business is likely to flourish over time if the demand for medium-term rental units continues to grow.

What Are the Cons of Managing a Mid-term Rental?

As with any business venture, there are certain aspects you need to be aware of if you’re going to be handling a mid-term rental, such as:

- Your property is more likely to be used for unethical activities. This is true of short-term and mid-term tenants but is slightly more common with short-term renters because they don’t plan on being there for very long and aren’t as invested in their community or neighborhood. If something unethical happens on your rental properties, it could lead to other issues like vandalism or noise complaints. To combat this, make sure your lease agreement clearly defines acceptable and unacceptable uses of the property, and be sure to screen your tenants thoroughly.

- If you don’t have experience managing mid-term rentals, it can be challenging to find the best tenants. However, there are digital tools you can use to market your listings efficiently. Make sure your rental application is easy to fill-out and professional to attract great tenants.

- There can be more legal issues in managing a mid-term rental than a short-term one. That’s why it’s so important to speak with your attorney or local housing authority before a lease is signed. You need to know the full scope of potential risks to determine if you want mid-term rentals to comprise a share of your real estate investing efforts.

Conclusion

Mid-term rentals offer fantastic opportunities for prospective landlords and seasoned property managers alike. With a wealth of prospective tenants and the flexibility of a shorter commitment, this type of lease can prove to be lucrative. Mid-term rentals are an interesting and exciting way to diversify your investment portfolio, just remember to speak with an attorney or housing authority to confirm mid-term landlord expectations.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

Listen On:

On this episode of the Your Landlord Resource podcast, we are interviewing Sarah King an investor and self-managing landlord.

She’s here to motivate and inspire you with her stories of triumph as well as hard times and how she nearly lost everything but did not let that setback hinder her goal of owning multiple rental properties.

Sarah also discusses that at some point or another, everyone will deal with some sort of problem in their rental property that is caused by water. Whether it be a water leak, or old pipes, clogged pipes, frozen pipes, or pipes installed incorrectly, you will find yourself scratching your head about issues with water and water damage.

Sarah has rebuilt her portfolio to include short term, midterm, and long-term rentals along with a few flips here and there. She has built a great team to support her directly with her rentals as well as developed a network of friends to keep her motivated through all the good and bad that owning and operating rentals throws at you.

We could not be more excited about interviewing Sarah to hear all about her landlording journey!

LINKS

👉 Episode 14: The Importance of a Rental Property Maintenance Team

👉 Episode 15: Developing Your Office Operations and Business Team

👉 Sarah’s book recommendation: The Simple Path to Wealth

👉 Follow Sarah on Instagram

👉 Sign up for Sarah’s Equity Partnership and Private Money Interest List

👉 FREE Download! Sarah’s Private Money Lender Pitch Deck

👉 Sarah loves Bigger Pockets! Sign up for a FREE account

👉 Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

👉 Help other DIY landlords discover what we have to say… Please leave us a review of our podcast!

On Apple Podcast or ITunes, please scroll to the bottom of our main page (with our logo) and click “Write a Review”.

On Spotify, please click the 5.0⭐ on our the front page of our podcast page.

👉 Join our Private Facebook Group! A space to ask questions and network with other DIY landlords.

👉 Follow us on Instagram

👉 Like us on Facebook

👉 Want the podcast link emailed to you weekly? Subscribe to our FREE newsletter, Landlord Weekly!

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

Check out samples of our newsletter👇 If you love it, you can subscribe from there!

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

Think you’ve got the best apartment community in your city yet struggling to retain residents? We get it. In the ever-changing landscape of apartment life, it’s not just about offering a great space; it’s about truly understanding what residents want and making their living experience effortlessly enjoyable.

Join us as we walk you through 7 creative ways to boost resident retention and, while we’re at it, elevate your apartment game.

Let’s not just make residents want to stay; let’s turn their satisfaction into glowing reviews that attract new residents to your thriving community. It’s time to create a living experience that keeps everyone excited to call your place home.

Let’s jump right in!

Why Resident Retention Matters

In the realm of apartment management, resident retention isn’t just a lofty goal; it’s a vital component that shapes the overall health and success of your community. Let’s break down why keeping residents around is more than just a numbers game:

Financial Impact

The cost of acquiring new residents can significantly outweigh the expenses of retaining existing ones. A revolving door of residents means constantly investing in marketing, paperwork, and the logistics of turnover.

Positive Reputation

A community with high resident turnover might be perceived as unstable or lacking in quality. On the flip side, a place with satisfied, long-term residents tends to build a positive reputation, attracting new residents organically.

Maintenance Efficiency

Regular turnover means more wear and tear on units. High resident retention translates to more predictable maintenance schedules and less frequent, large-scale refurbishments.

Word-of-Mouth Referrals

Happy residents become your best ambassadors. They’re more likely to recommend your community to friends, family, and colleagues, creating a stream of qualified referrals.

All in all, resident retention isn’t merely about keeping units occupied; it’s about nurturing a thriving, interconnected community that benefits both residents and management alike. So, let’s get started on 7 creative ways to boost resident retention at your apartment community!

7 Creative Ways to Boost Resident Retention

Elevate Your Online Presence

In a world where digital connectivity is at the forefront, delivering a seamless online experience is key to boosting resident retention. Start by ensuring your website is not just a digital placeholder but a user-friendly portal that residents can navigate effortlessly.

An easy-to-use website and online portal streamline communication, making it simple for residents to access essential information, submit maintenance requests, pay rent online, and stay informed about community events.

Get Social

In the age of hashtags and shares, social media is a powerful tool for community engagement. Elevate your resident retention game by investing time and effort into creating meaningful content on your social media platforms. Share updates on community events, spotlight resident stories, and offer glimpses into the vibrant life within your community.

Just as important, don’t just broadcast; engage with your audience. Respond promptly to comments, encourage residents to share their experiences, and foster a sense of community online.

Improve Communication

Improving communication in your community isn’t just a pleasant add-on; it’s a game-changer that seriously impacts resident retention. Here are a few ways you can improve your communication with residents that will leave a lasting impact:

- Actively seek input from residents through surveys, suggestion boxes, or community meetings. Encourage open communication to understand their needs, concerns, and suggestions. Utilize feedback to make informed decisions that enhance the overall living experience.

- Ensure that all communication, whether written or verbal, maintains a positive and friendly tone. Approach resident interactions with empathy, addressing concerns with a solution-oriented mindset.

- Keep residents informed through regular updates on community news, events, and any relevant changes. Offer accessible resources, such as online platforms or newsletters, to provide useful information.

Need a Lease Agreement?

A FREE account gets you access to over 200 free forms. Upgrade to a paid account (monthly, annually, or lifetime)

EZLandlord Forms Is Offering 15% 𝙊𝙛𝙛 For New Customers!

We cannot recommend these guys enough!

👉 State Specific Leases 👉 400 Forms to make your landlord-tenant relationship top notch 👉 200 FREE forms for those not ready to purchase 👉 4.8 Rating with over 5000 Reviews 👉 Pro Members get access to ALL leases and forms for $12 per month OR $75 if you purchase the annual membership 👉 YOU CAN BUY LIFETIME FORMS for $399

USE CODE 𝐒𝐓𝐀𝐂𝐈𝐄𝟏𝟓 to get 15% OFF ALL first-time purchases, EVEN THE LIFETIME FORMS!

VIP Treatment

When it comes to advice for lease renewals, consider adding a touch of VIP treatment. Express gratitude to residents extending their stay with special perks or exclusive discounts, turning the renewal process into a positive experience.

This thoughtful approach not only shows appreciation but also plays a vital role in significantly boosting overall retention rates within your community.

Team Shoutouts

Implementing an employee recognition program in property management is more than acknowledging hard work; it’s about spotlighting the stars of your team. Celebrate their efforts on your social platforms or newsletter to showcase the faces behind exceptional service.

This boosts team morale and creates a connection with residents, ensuring a friendly atmosphere and enhancing the overall resident experience. Remember, happy and recognized team members contribute to a thriving community!

Keep Up with the Times

Staying up-to-date with the latest tech isn’t just a trend; it’s the key to giving your residents a happy home. From cutting-edge security systems to smart home features and super-efficient maintenance apps, the right tech not only makes daily life a breeze but also fits seamlessly with modern expectations.

It’s about creating a seamless, integrated experience, where technology fosters community engagement, supports sustainability, and nurtures a sense of belonging.

Choosing the right tech mix is crucial – ensuring they all integrate seamlessly, avoiding conflicts, and creating a harmonious, tech-forward environment that keeps residents content and connected.

Community Events

Life’s better when it’s shared, right? That’s why hosting regular community events is a great way to make residents feel more connected to your community.

Whether it’s a laid-back free coffee morning, a holiday-themed party, or an educational workshop, these events aren’t just about filling your calendar. They’re about bringing everyone together, fostering connections, and creating a community that feels like family.

Because who wouldn’t want to stick around where there’s always something exciting happening?

In the dynamic world of apartment living, keeping residents connected to your community goes beyond square footage – it’s about crafting a true home experience. We’ve laid out 7 unique ways to turn your community into a place where residents don’t just stay; they thrive.

From a user-friendly website to VIP treatment during renewals, these aren’t just tips; they’re keys to personalizing your community. Recognize your exceptional team, embrace tech trends, and throw events that turn neighbors into friends.

Source: Multifamily Insiders

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

The surest way to derail any real estate business is a failure to protect yourself and your assets. Insurance isn’t the most exciting topic, but if you don’t properly cover yourself, your corporate entity, and properties, you can put your entire financial well-being at risk.

Landlords require a different type of insurance product than regular homeowners, and even then, there are nuances to be aware of depending on your particular situation and location. Today, we will demystify some of the most important aspects of landlord insurance to ensure you and your assets are protected.

Disclaimer: All real estate investors must discuss their unique situation with a licensed and experienced real estate insurance broker. The content of this article is for informational purposes only, and should be used in conjunction with advice from an insurance professional.

Difference between homeowner and landlord insurance

As a landlord you require landlord insurance instead of owner-occupied homeowner insurance. If you’re running a rental property business, there are additional protections that you should ensure you have in addition to what a primary residence homeowner may need. A homeowner policy will cover standard liabilities such as fire, flood, personal belonging protection, theft, among others. While many of these are important for real estate investors, there are additional protections you may require.

As a landlord, you will not need to insure the contents (personal belongings) of your units, that will be the responsibility of your renters—many landlords make this mandatory. That said, you may need additional coverages such as income loss coverage in case of loss of rental income resulting from flood, fire, or significant tenant damage to your property.

Landlord insurance 101

There are three standard insurance policies that landlords should be familiar with: DP-1, DP-2, and DP-3. The standard DP-1 policy generally covers less than DP-2, and DP-3. For instance, DP-3 policies cover most perils such as theft and vandalism and liability coverage, whereas DP-1 and DP-2 may not. In the case of liability coverage with DP-3 policies, if a tenant injures themselves on your property you can then turn to your policy to cover legal or medical expenses.

As noted above, most landlord insurance policies don’t cover the contents of the units—this is the responsibility of the tenant. That said, most DP-3 policies cover landlord-owned contents, such as appliances or furniture. DP-3 policies also include loss of rental income, meaning if the unit is off-market while you make repairs. Here are some of the common insurance policy features you’ll want to consider:

- Property protection (structure)

- Personal property protection (contents)

- Liability

- Rental loss protection (only if the unit is unhabitable for various reasons)

- Flood

- Acts of nature (be sure to ask your broker what is covered, and what isn’t)

Rental Loss covers lost income when the property becomes uninhabitable and does not typically protect against tenant default or vacancy. You can buy additional insurance to cover tenant default, which may be worth considering if you can’t cover your mortgage without the rental income and if you think it will be hard to find a new tenant and/or difficult evict a tenant who is withholding rent due to no fault of your own.

It’s worth noting that if you have an HOA, there will be insurance associated with the ownership structure of the HOA. For instance, a condo building with an HOA will have their own insurance to cover certain things. In this case, it’s important to work with your broker to ensure you aren’t doubling up on coverage that is already under an HOA policy.

My pre-paid policy doesn’t expire for many months?

Don’t worry, you can switch insurance providers at any time and you will get a prorated refund for unused coverage. Talk to your insurance broker or a new insurance provider for the details. Don’t let your current policy hold you back!

So what is the cost of landlord insurance?

The general rule is that landlords can expect to pay roughly 15% more for landlord insurance than a standard homeowner policy. According to Insurance.com, the national average cost of a homeowner policy is $1,288. Therefore, most landlords can expect to pay roughly $1,481 a year for landlord insurance.

The higher cost is because insurers are taking on additional risk for landlord insurance because of the presence of renters. Here are some other factors that affect the price of your landlord insurance:

- Security features

- Age and condition of the property

- Smart home devices that provide early warnings of potential issues

- Number of rental units

- Location

- Safety equipment on the premise

- High-risk features such as wood fireplaces, pools, and hot tubs

- Long-term vs short-term tenants (different coverage is needed for each case)

Your Landlord Resource has teamed up with Toggle, a division of Farmers Insurance that offers competitive pricing of renters insurance for tenants.

Policies can start as low as $5 a month!

Copy and share our link with your tenants to get them started: http://go.gettoggle.com/SH1E

Download this PDF to present to your tenants with your renters insurance request! Toggle Renters Insurance Flier.pdf

Questions to ask your insurance broker

It is critical that you speak with a licensed insurance broker prior to purchasing any rental property. You should also obtain insurance quotes. Consider using a broker if you don’t already get a packaged deal from an insurance provider because brokers can shop around for the best prices and policies. A single insurance provider however may give you a bulk deal if you work only with them. Be sure to explore both options.

Not only should insurance be a part of your investment due diligence, but many lenders also require it as part of the financing process. When speaking with your broker, here are some questions that may be worth asking:

- Are there any upgrades/repairs I can do to this property to reduce my insurance costs?

- Does this policy cover flooding, and what type of flooding (natural disaster vs sewer backup vs tenant error)?

- What are all the deductibles on my policy?

- Are there additional coverages I should add on given my location?

- Are there any insurance discounts that may apply to my situation?

- Does my policy cover both short and long-term rental periods?

- What if my property is damaged by the negligence or criminal acts of my tenant?

- How is the replacement cost or cash value calculated under this policy?

- Does my policy cover other structures on my property such as a shed or coach home?

- Should I get a separate umbrella policy to cover myself if I max out my liability coverage?

- Will having safety equipment on premises reduce my landlord insurance premium?

- What is NOT included in my landlord insurance?

- Is my policy covered in the event of a terrorist event?

Be sure to conduct your due diligence with your insurance broker, and speak with other landlords in your area to better understand the most common scenarios that could arise.

6 critical tips when seeking landlord insurance

Tip 1: Make it mandatory for your renters to have renters insurance. You can make this a part of the application process, or ask them for proof of a renter insurance policy when they sign the lease. Thankfully for tenants, the renters insurance cost is quite low, and can run as little as $20 a month.

Tip 2: Consider going with the same insurance provider for all your rental units to get a bundled discount.

Tip 3: Add short-term rental coverage to your insurance policy to give yourself the flexibility to rent out your unit for short-term periods if needed.

Tip 4: If you have a net worth that is higher than the liability coverage on your insurance policy — $1 million for example — you should consider getting a separate policy to cover yourself or LLC if you require more coverage if needed. For instance, if your liability coverage is only $1 million but your net worth is $5 million, you don’t want to max out your liability coverage and then leave you personally liable for the remainder. You can obtain a second policy that will cover your assets should this be the case.

Tip 5: Make sure your rental loss coverage is the same as your gross rents for the entire dwelling to ensure there is zero loss of income.

Tip 6: Consider add-on insurance items if they aren’t on your current policy such as flooding, wildfires, burglary, earthquakes, terrorism events, and vandalism.

Final thoughts

There’s no doubt that adequate insurance coverage can make or break your real estate investing business. If 10 years ago there was flooding on your street and sewers backed up, then you need to ensure you have that coverage. Further, if a tenant slips and falls on the steps and you’re held liable but don’t have any liability coverage, you’re putting your business and personal finances at risk.

Get different quotes, speak with experts in the area like local insurance brokers, and conduct your due diligence alongside a professional insurance professional. That way, you can go to sleep at night knowing that no matter what happens, you and your business will be covered.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

In most states, landlords are required to give tenants 30-60 days’ written notice before selling their rental property. This is to allow tenants sufficient time to find a new place to live and move out.

As a property owner, you may decide to sell your rental property for various reasons, such as retirement or relocation. However, it’s crucial to notify your tenants early to avoid causing them any inconvenience or financial hardship. In some cases, you may need to terminate a lease agreement early if the tenant’s lease has not yet expired, and you want to sell your property.

It’s important to know the legal requirements and obligations for providing notice to your tenant and terminating the lease agreement without any legal disputes. We will explore how much notice you need to give a tenant when selling your rental property.

How Much Notice Do You Need To Give A Tenant When Selling: A Comprehensive Guide

Understanding Tenant Rights When Selling: Why Proper Notice Is Necessary

When it comes to selling a property that has a tenant, there are a few important things to keep in mind. First and foremost, you need to understand the tenant’s legal rights and the notice requirements when selling.

Proper notice is necessary to avoid any legal issues and ensure a smooth transition.

Here are a few things you need to know:

- A tenant has the right to remain in the property until their lease expires, even if the property is sold.

- A tenant cannot be evicted or asked to leave the property solely because it has been sold.

- A tenant has the right to know when the property is being sold and who the new owner will be.

- Failure to give proper notice to the tenant can result in legal and financial penalties for the landlord.

Statutory Notice Requirements: The Basics Every Landlord Needs To Know

As a landlord selling a property with a tenant, it is important to be aware of the statutory notice requirements in your state or territory.

he notice period will depend on the type of tenancy agreement and the location of the property.

Here are the basic notice requirements every landlord needs to know:

- In most states, landlords must provide written notice to their tenants at least 30 days before the end of the lease agreement if they do not want to renew the lease.

- If the tenant is on a fixed-term lease, the landlord cannot ask them to vacate the property until the lease has expired.

- If the tenant is on a periodic tenancy, the landlord must give a written notice period of 60 days.

- In some jurisdictions, landlords must inform tenants in writing about the impending sale of the property.

Exceptions To The Rule: When Notice May Not Be Required

- In some situations, a landlord may not be required to give notice to their tenant before selling the property. Here are a few exceptions to the rule:

- If the tenant is on a month-to-month tenancy, the landlord can terminate the lease by giving a written notice of 30 days before the end of the month.

- If the property is being sold to another landlord, the tenant’s lease may transfer to the new owner, and notice may not be required.

- If the tenant breaches any of the terms of their lease, the landlord may be able to terminate the lease early and sell the property without notice.

Giving proper notice to a tenant when selling a property is not only legally required but also the right thing to do.

As a landlord, it is important to understand the tenant’s rights and the notice requirements to avoid any legal issues and ensure a smooth process.

By following the statutory notice requirements and knowing the exceptions to the rule, landlords can sell their properties with peace of mind.

Estate Planning You Can Trust

Simple. Easy. Trusted.

Nolo’s WillMaker is America’s #1 estate planning software. Get immediate access to easy-to-use software and create your customized will today. Make a living trust, healthcare directive, power of attorney and so much more. There’s never been an easier, more affordable way to protect your family, home and assets.

The Legal Aspects Of Giving Notice To Tenants Before A Property Sale

As a landlord planning to sell your rental property, one of your obligations is to give notice to your tenants before selling.

In many cases, it is a legal requirement to serve written notice and adhere to other legal formalities.

Here’s everything you need to know about the legal aspects of giving notice to tenants before a property sale.

Types Of Notice: Which One Is Right For You?

The type of notice you serve the tenant depends on the location and situation. Here are the different types of notice that you can use before selling your rental property:

- Written notice to quit: This notice is used when you want the tenant to vacate the rental property, and it is commonly used when the rental property is being sold in a non-tenant-occupied unit. In some states, the notice must be served at least 30 days before the property’s sale.

- Written notice of intent to sell: This notice informs the tenant that the property will be sold and advises the tenant of their rights regarding the sale. You usually send this notice if you intend to sell the property with the tenant in place.

- Notice of sale: This notice is used when the rental property is being sold to a new owner, and the tenant’s lease will be assigned to a new owner. It notifies the tenant that the property is sold and informs the tenant of the security deposit’s transfer.

How To Draft A Proper Notice Of Intent To Sell

Drafting a proper notice of intent to sell is essential to make sure you remain within the law. Here are the crucial aspects to consider when drafting a notice of intent to sell:

- Include the tenant’s name, property address, and any other identifying information.

- Mention the date the notice was served.

- Explain the terms of the sale, such as the closing date, the new owner’s name, and the buyer’s intent for the property.

- Include your contact information, so the tenant can contact you with any questions or concerns.

Delivering Notice: Best Practices And Common Mistakes To Avoid

After drafting the notice, delivering it to the tenant is equally vital. Here are the best practices to follow:

- Make sure you deliver the notice by hand or mail, whichever is agreed upon in the lease or mandated by state law. Email or phone call is not acceptable in most cases.

- Keep a copy of the notice, including the proof of delivery.

- Be friendly and straightforward when speaking to the tenant. Explain the terms of the sale and how it will affect their tenancy.

- Adhere to state law and lease agreement requirements for serving notice.

As a landlord, it is your duty to give notice to your tenant about selling the rental property.

Understanding the type of notice, drafting a proper notice and delivering it according to state law, and best practices is crucial for a smooth sales process.

Frequently Asked Questions

What Is The Notice Period When Selling A Rental Property?

The minimum time period is usually 30 to 60 days in advance.

Can You Show The House To Potential Buyers During The Notice Period?

Yes, as a landlord, you have the right to show the property to potential buyers.

What Happens If The Tenant Doesn’t Leave After The Notice Period Ends?

You can seek legal help to remove the tenant or offer them a new rental agreement.

Is There Anything Else To Consider When Giving Notice To Tenants When Selling?

Make sure to provide a written notice, communicate with the tenant, and keep records of the notice.

Conclusion

Providing notice to tenants when selling a property is an essential step that should not be ignored.

As a landlord, being transparent and communicative with your tenants can assist you in avoiding any legal conflicts. Additionally, it may help ensure that you successfully sell your property.

By following the guidelines set by state and local laws, you can adequately provide notice while respecting your tenants’ rights.

Remember to provide enough time for your tenants to make arrangements and find new accommodations.

Selling a property can be a stressful experience, but taking the necessary steps ensures a smooth transition for yourself and your tenants.

By prioritizing your tenants’ needs, you can maintain a respectful and professional relationship that may benefit you in the future.

Overall, providing notice to tenants is a crucial aspect that should be carefully considered when selling a property.

Source: Rental Awareness

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

Listen On:

So, way back we did an episode discussing the pros and cons of whether holding your rental property in an LLC is right for you or not. Well, we had a lot of requests asking us to talk about the actual process of transferring your rental property into an LLC and now here we are discussing it.

It may seem like a very cut and dry concept, and for the most part it is, but there is quite a bit to know about the process before you take the steps to make that transfer.

Things like, will your mortgage lender allow it? What if my rental was purchased with a 1031 exchange that was titled in my personal name? What forms do we need to use? Or how will the process affect getting loans on future properties?

We are using personal stories of our transfers to help you get a clear understanding of why we did or did not choose to transfer our rentals to an LLC. Plus, we tried our best to keep it as simple as possible so you can have a clear understanding of what transferring your real estate investments into an LLC entails.

LINKS

👉 Episode 16: Is Holding Your Rental In An LLC Right For You?

👉 NOLO Legal Forms: Make your business an LLC

Structuring your business as an LLC can bring important advantages: It lets you limit your personal liability for business debts and simplify your taxes. Here, you’ll find the key legal forms you need to create a single-member or multi-member LLC in your state, including:

• LLC articles of organization

• operating agreement for member-managed LLC

• operating agreement for manager-managed LLC

• LLC reservation of name letter, and

• minutes of meeting form.

Form Your Own Limited Liability Company has easy-to-understand instructions, including how to create an operating agreement that covers how profits and losses are divided and major business decisions are made. You’ll also learn how to choose a unique LLC name that meets state legal requirements and how to take care of ongoing legal and tax paperwork.

Launch Your LLC Today!

👉 Course Waitlist: From Marketing to Move In, Place Your Ideal Tenant

👉 Help other DIY landlords discover what we have to say… Please leave us a review of our podcast!

On Apple Podcast or ITunes, please scroll to the bottom of our main page (with our logo) and click “Write a Review”.

On Spotify, please click the 5.0⭐ on our the front page of our podcast page.

👉 Join our Private Facebook Group! A space to ask questions and network with other DIY landlords.

👉 Follow us on Instagram

👉 Like us on Facebook

👉 Want the podcast link emailed to you weekly? Subscribe to our FREE newsletter, Landlord Weekly!

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

Check out samples of our newsletter👇 If you love it, you can subscribe from there!

*This post contains affiliate links. We may earn a very small commission (at no additional cost to you) if you purchase from here. These small commissions are to benefit our business so thank you for your support.

By Ryan Squires

One of the biggest allures of investing in rental properties stems from decreasing an individual’s taxable income through rental property depreciation.

As we all know, building wear and tear has real costs. As structures wear out over time, the usable life and value of that property decreases. Those decreases can be accounted for using the IRS’ guidelines on the depreciation of rental property.

For savvy real estate investors and landlords, accounting for a rental asset’s decreased usability minimizes tax liability by shrinking taxable income. If done right, landlords can keep more money in their bank accounts.

However, accounting for depreciation costs, while a wise financial move, can be a time-consuming and complex process. With that in mind, we’ll examine rental property depreciation, how to calculate it, and some tools investors can use to alleviate stress during tax times.

What is rental property depreciation?

Rental property depreciation is a tax law concept that allows rental property owners to deduct a portion of the cost of a property and any improvements they make over a set period, generally 27.5 years, as defined by the General Depreciation System (GDS), which we discuss in further detail below.

The total number of years, 27.5, represents a key figure because that’s what the IRS deems as the usable life of a residential rental property when using GDS. Instead of taking one large deduction for the entire cost of the property in the year you buy it, depreciation allows investors to deduct a smaller amount each year to account for wear and tear.

Note: While GDS is the most widely used system, the IRS also employs the Alternative Depreciation System (ADS), which we explain in our Calculating Depreciation section.

Is your property a depreciable asset?

Your property must meet four essential criteria to be eligible for depreciation based on IRS guidelines.

- Landlords and real estate investors must own the property, and they’re still considered the owners if they owe on it.

- Investors must use the property to generate income.

- The property must have a “determinable useful life.” The IRS defines properties as having a useful life if they can “wear out, decay, get used up, become obsolete, or lose value from natural causes.”

- Investors can only claim depreciation on properties with a useful life of more than one year.

For properties that fit these parameters, investors can then determine how to calculate their depreciation values to factor into deductions.

Calculating Depreciation

One of the biggest aspects of rental property depreciation is determining when to start depreciating a property, which is when it’s placed “in service.” When buying a new property, investors often face many challenges related to making it habitable or appealing to potential tenants.

That could mean fixing broken fixtures, repairing structural components, or upgrading appliances. Suppose an investor purchases rental property on February 1, but it requires them to put some work into it, which delays advertising the property until March 15.

In this case, the in-service date would be March 15. However, landlords can still depreciate the property from that date, even if they don’t have a tenant.

Now that you know when to begin depreciation, you must determine which depreciation system to use. Don’t worry — it’s not that hard.

Depreciation Methods

Investors whose rental properties were placed in service after 1986 will use the Modified Accelerated Cost Recovery System or MACRS.

MACRS uses two depreciation methods — the GDS and the ADS — which we briefly mentioned above. Let’s examine the two systems in more detail to determine how they apply to rental property depreciation tax accounting.

General Depreciation System

GDS is the most commonly used depreciation method, so investors will likely use it when depreciating their rental properties. It outlines some fundamental principles.

As previously explained, depreciation for residential rental properties is commonly spread over 27.5 years. In effect, this implies that investors and landlords can benefit from significant tax deductions at the early stages of ownership. Commercial properties, on the other hand, use a 39-year depreciation window.

Second, GDS primarily uses the straight-line method of depreciation. That means investors will always deduct the same amount from their taxable incomes based on the cost basis, which we discuss below.

While the straight-line method is the most commonly used, it isn’t the only one landlords can use in this system. Investors can also use the declining balance method, which allows for larger deductions in the early years.

Alternative Depreciation System

Fewer landlords will use ADS. The IRS stipulates that real estate investors and landlords must use the ADS rental property depreciation system if certain conditions are met.

You must use the ADS system in the following cases:

- The property has a tax-exempt use

- The property uses tax-exempt bond financing

- The property is used primarily for farming

- The property is used for business purposes for 50% or less of the year

If your property fits those descriptions, you‘ll employ ADS. ADS uses a longer depreciation schedule of 30 years. This schedule lowers depreciation deductions and spreads them out over a longer period.

Keep in mind: Landlords and investors can opt to use ADS for their properties on a unit-by-unit basis, but once they select the ADS method, they cannot change it.

Check out the IRS documentation linked above for more information on either schedule.

Calculating Cost Basis

Now that we’ve specified which depreciation method applies to a given property, finding the cost basis of a property will give you all the information needed to determine the values you can deduct from your taxable income.

The first step is to determine the property’s cost. For example, say you find a property listed for $418,000. Often, that’s not the final price. You may need to add in settlement costs or fees directly incurred at the time of purchase, such as legal fees, transfer taxes, title insurance, and any additional fees you agree to pay. Let’s ascribe a value of $15,000. You capitalize or add these to your depreciable cost basis in the property.

Now, suppose you renovated the kitchen for $30,000 to make the property more appealing. You can add these costs to the basis to help offset the initial investment. In short, the total cost of acquiring the property and renovation is $463,000 ($418,000 property price + $15,000 in fees + $30,000 renovation).

You can’t depreciate the entire $463,000 because the building sits on land, and that can’t be depreciated. The IRS states that land isn’t a depreciable asset as it has an indefinite use life, so you’ll subtract the land value from the total purchase price. When you segregate out the cost of the land and tally up the other values, you arrive at your depreciable cost basis. You’ll use this figure to calculate your depreciation expense each year.

A landlords one stop shop for tenant management…for FREE

You can’t beat free and the only time you pay is if you want to purchase a lease or have expedited rent deposits. Most everything else costs zip, zero, zilch.

Establishing Land Value

Investors can find the value of land from a number of sources to help in their rental property depreciation calculations, including:

- Property tax card or bill: Local governments often assess the value of the land and the building separately for property tax services. This information is readily available through your assessor’s website or office.

- Assessed values: Your property tax documentation should show the value assigned to the land and the building improvements separately.

- Professional appraiser consultation: Hiring an appraiser can help streamline the process and ensure a property appraisal if the tax assessment seems inaccurate.

Final Calculation

Say the appraiser values the land at $40,000. If using GDS, subtract $40,000 from the cost of acquiring and renovating the property ($463,000) and divide it by 27.5 years.

For example: $463,000 – $40,000 = $423,000. Divide that by 27.5 years, and you get $15,381.82 which you can now deduct from your annual income. However, for the first year you put the property in service, you’ll consult the MACRS percentage table to calculate the depreciation deduction based on the month you placed the property in service.

According to the percentage table, if you put the property in service in July, you’ll depreciate at 1.667%. Here’s the total for the first deduction: $423,000 (cost basis) * 1.667% = $7,051.41. This is because you’re only allowed to claim a half-year worth of depreciation on this first year.

When Depreciation Stops

Once the property changes hands, the 27.5-year clock starts anew. However, there are other circumstances when investors can no longer deduct rental property depreciation from their taxable income.

The first is when the property has fully recovered its cost. That means an investor has deducted the property’s entire cost basis.

The other is when the property no longer generates income. For example, an investor could move into the property, taking it off the rental market altogether and ceasing income generation.

Recapture Considerations and Capital Gains

While depreciating properties comes with substantial tax deductions, you must pay some back via recapture taxes, which the IRS levies at tax time each year after the year of sale. Also, if you don’t plan on reinvesting your gains via a 1031 exchange, you’ll have to pay capital gains tax.

Let’s look at an example to see how the numbers work out.

Assume you purchased the property above six years ago and sold it at the end of the sixth year for $700,000. In our example, we determined the property had a cost basis of $423,000. Because you sold the property after six years, the depreciation deductions you’ve taken amount to $92,290.92. Now, you’ll have the figures necessary to calculate the property’s adjusted basis.

To calculate that amount, subtract the $92,290.91 in accumulated depreciation deductions you’ve claimed on your taxes from the original cost basis of $423,000 for a total of $330,709.09. Now, subtract the adjusted cost basis from the sales amount of $700,000 ($700,000 – $330,709.09 = $369,290.91).

Of that $369,290.91, $92,290.91 is taxed at your ordinary income tax rate, which is not to exceed 25% as outlined in the Tax Cuts and Jobs Act. The remaining $277,000 is then taxed at your long-term capital gains tax rate of 0%, 15%, or 20%.

Long story short, while investors benefit from tax reductions during their property ownership, it’s vital to account for recapture and capital gains taxes to understand your finances following the sale of a property.

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇

Naming apartments is a tricky game—and creating it to be one-of-a-kind is the NAME of the game, pun completely intended.

What Can an Apartment Name Do?

The purpose of a name? It’s shorthand for who your brand is. It gives a snippet of an idea. A name is the first thing that can grab attention (if it’s a good one), keep attention, and if it’s interesting enough, it can allow the prospect to ponder its meaning a little bit.

Your apartment name can tell a story, evoke a feeling, and emphasize your branding—when you follow our guidance.

TELL A STORY

Names that make for the most fun in the process are the ones with a story. If there isn’t one, we create it within the brand guidelines. Have you ever met someone with such a unique name that you wanted to say, “Wow, that’s cool! Can you tell me more about your name?” There’s typically something even more interesting than the name—and it’s the story behind it.

EVOKE A FEELING

The vibe of your community—whether for retirees or for young professionals—will be bolstered by a solid name. There are certain sounds, colors, words that create ideas and stir up emotions within us. The emotions that come to the surface should be positive. Positive and fun. Positive and elegant. Positive and avant-garde. Positive and peaceful. How you name it helps bring your reader/prospect/resident to that frame of mind.

EMPHASIZE BRANDING

The vibe of your community again can be paired up with your branding through your apartment name. The name is the starting point, and then the brand is built up around that. It’s likely that you’ve already had the ideas of the design, style, audience and more, but the name is the first piece of the verbal branding. This aspect is foundational, setting off the rest of the branding: your logo, your style, your voice, so it can be seen and appreciated in its ideal form.

Why One-of-a-Kind Names for Apartments?

Naming your apartment buildings is not a decision you can make easily and forget about. It will impact your brand perception, how prospects find you online (or don’t) and whether your brand will stand out among your competition. Be careful in your approach to naming apartments for both SEO and intrigue.

SEO

If you want to be found through search engines, consider how many other things, even beyond apartment communities, may be named the same. How much competition will you have? A lot? This is the time to get inventive, because it won’t always go the way it did in Field of Dreams (“If you build it, they will come.”)

Now, does it have to be a completely new word? Not necessarily. But for higher ranking in Google, it must be more creative and outside of the norm.

Please don’t call it Oakview or Oakhill or Oakridge or Oak Grove Apartments. It’s been done.

INTEREST

Look for something more interesting about the property to inspire its name. Perhaps the history of the area, the street names, important figures in the city’s community, or a particular vibe that you want to create with these apartments.

MEMORABILITY

If it’s top-of-mind status you want, you’ll have to go a little off the beaten path. Not too strange, and not too un-spell-able or un-pronounce-able, but something that’s creative. So instead of Oakhill Apartments, you could go for CenturyWood Place, for example.

Never Pay for Covered Home Repairs Again.

Choice Home Warranty is the most comprehensive, flexible, and value-priced on the market.

Get local pre-screened technicians, if we can’t fix it, we’ll place it, and receive 24/7 home warranty service.

Apartment Name Examples

Now that we gave you one example, you’re probably hoping for a few more. We got you. (Keep in mind that these are all made up and we aren’t picking on anyone with these examples, good or bad.)

BORING

That Oak Anything Apartments example falls into this boring category. Not imaginative. Sounds peaceful and completely…forgettable. Here are a few more apartment names that you can forget about completely after reading them:

31st St Apartments

Oak Glen

Shady Lane

Laurel Estates

We get it: There’s shade. You’re on a street. There’s trees. For the love, get more interesting!

UNIQUE

Take inspiration from the management’s founder. The history of the area. Or the style of the building. Don’t be too on the nose, like Brickhouse Lofts, but consider using a red color in the name, like Vermillion Views.

THE STRANGELY FAMILIAR

Today, there are plenty of made-up words that have become household names—even regular, daily verbs. Why? Because they’re memorable. Just Google it!

Google was a re-spelling (which was more phonetically appealing) of googol, which just means the highest number in existence. This works great for the vast number of search results you can receive with a few keystrokes.

Etsy was a made up spelling after the founder closely watched (and listened to) a Fellini film. Having heard “et si” multiple times, he decided this combo of words that means “oh, yes” was the perfect term for his new website.

Zillow is a little more out there. This massive house listing giant has combined the idea of comfort and vast amounts of options (“zillions” and “pillows”—where you lay your head) would be the ideal name for a space to find your next property.

What to Consider When Naming Apartments

As we’ve seen above, some brand names are more thought out than others. It’s okay if it’s stumbled upon, but it’s stronger and more relatable if there’s a good story to go with it.

MEANING

Why is it called that name? If it’s chosen at random, that’s not going to initiate very good conversations. If you can come up with history, inspiration, or reasoning, that will go a lot farther in your branding guidelines than “it sounded cool.” However, we know that sometimes that does lead to success. But it might be easier to have a goal to create a name based on some deeper meaning–it’s at least an easier starting place.

BRAINSTORMING PROCESS

Thinking through naming apartments, go for broke. We write down anything and everything that comes to mind, and then have a thesaurus handy. (You never know when you’ll come up with something that will spark interest and be super-original.)

While we’re going about the naming process, we consider things like:

- Your ideal resident profile (IRP): what are they looking for?

- The type of apartment community it will be

- The vibe of the surrounding area

- The history of the town/city/area you’re in

- The history of the building

- The architecture style of the building

- The names of the surrounding streets

- The local flora and fauna

Take all of these into account, and we’re sure to find something that will strike a chord that will please the SEO gods and the future residents of your homes. We’ll also try out different sizes, lengths, and formats of the winsome ones to land on something worthy of your community. Most of all, we’ll aim for meaning and originality.

RESEARCH

However, before you get too deep into the weeds of apartment naming, make sure it’s actually viable. Look at your competitors. Consider your audience. Google the name and see what comes up. A few considerations (or tests, if you will) to find out whether the name could possibly work:

- Business Name Search

- Trademark Registry Search

- Available URLs and social media handles

- General Google search

Again, this is where due diligence and uniqueness will help you out. The hard work of building your apartment brand will be undercut by other brands if it’s not a standalone idea (or has too much competition).

Source: Multifamily Insiders

Did you enjoy this article?

This is an example of what is included on our FREE weekly newsletter, Landlord Weekly.

Subscribers get access to our free forms, email templates, and guides! As well as…

▪️Landlord Tips ▪️ Early Access to Our Blogs ▪️ Landlord Specific Articles by Other Industry Pro’s ▪️ Podcast Links

To check out a sample of our newsletter, click one of the links below👇